Personal pension providers’ readiness for pensions dashboards

Executive summary

This report presents the findings from the preparation for dashboards survey of Financial Conduct Authority (FCA) regulated pension providers.

Ipsos conducted an online survey with FCA regulated firms to understand how they are preparing to connect to the pensions dashboards central digital architecture and respond to find and view requests. In particular, what preparations are being made and how; what dates firms are planning to connect by; their confidence around being ready to connect according to the connection guidance schedule.

Online fieldwork took place between 9 October 2024 and 6 November 2024. The Pensions Regulator (TPR) has been running a similar survey for their regulated occupational pension scheme trustees. Invites to take part in the survey were sent via email. Four reminder emails were sent out during the fieldwork period.

The findings show high awareness of pensions dashboards among the FCA-regulated firms that responded to the survey. Many are actively preparing for connection, although there are variations in preparedness, particularly between large and small firms.

Most firms are aware of their pensions dashboards duties

- Overall, most firms who completed the survey had both read the DWP’s guidance Pensions dashboards: guidance on connection: the staged timetable, and reported knowing their ‘connect by’ date (95% respectively).

- Firms’ engagement with legislation and guidance was high. Nearly all firms (97%) reported that they had read the FCA’s Policy Statement 22/12: pensions dashboards rules for pensions providers, or the Pensions Dashboards Programme (PDP) draft standards and guidance (92%). A slightly lower proportion of small firms (those administering less than 5,000 pensions pots) were likely to have read the PDP guidance (82%) compared to 100% of large firms (those administering 5,000 or more pension pots).

- Smaller firms were less likely to have accessed the PDP connection hub (59%) compared to large firms (84%).

Almost all firms are already undertaking preparations to connect

- Overall, most firms (83%) reported that they intend to connect by their ‘connect by’ date in the DWP guidance.

- Most firms intend to connect to the central digital architecture using third-party suppliers (82%). Very large firms (more than 500,000 pension pots) were much more likely to connect directly (38%), but the base size for this group is very small.

- Of the small proportion of all firms who intend to connect directly (10%), most have already begun building an interface and are already engaging with PDP about their interface.

- Of those intending to use a third-party supplier, most intend to use an existing supplier (65%), whilst just under a third of all firms (31%) intend to procure a new supplier.

- Of those firms that intend to procure a new supplier, a majority had already completed the process (61%), whilst all others expect to have done so within the next 6 months (39%).

- Large firms (those firms likely to have an April 2025 ‘connect by’ date in guidance) were generally more advanced than small firms (those firms likely to have a January 2026 ‘connect-by’ date in guidance) in terms of preparation.

- Overall, firms were broadly confident that they would be able to meet the different standards by their ‘connect by’ date. However, firms reported different levels of confidence for different actions.

- Firms reported higher confidence that they would have implemented their decisions on which personal and contact data items they will be using for matching members to their records by the ‘connect by’ date with over three-quarters of all firms (80%) reporting to be completely/very confident. This compares to 67% of all firms who were completely/very confident they will be able to provide timely, accurate and sufficiently up-to-date value estimates for all pensions.

- Firms were also largely confident that they would have fully digitised and accurate data for matching customer records, with 97% of surveyed firms expressing some degree of confidence. Most (75%) reported being either very (37%) or completely (38%) confident, whilst a further 22% reported being fairly confident.

Most firms already hold the relevant customer data in digital format

- Over three-quarters of all firms (78%) already hold all their customers’ data in a digital format and most firms (62%) know what data items they will use for matching.

- However, few firms are completely confident (24%) in the accuracy of their data, though most had plans to improve that accuracy.

- Most firms had matching/personal contact data in a digital format for all their customers (82%). A slightly larger proportion of small firms had all this data digitised (88%).

- Over half of all firms reported having 100% of their money purchase/defined contribution (DC) data regularly calculated and immediately retrievable. For data that is not, most firms intend to calculate values on demand to return within a 3-day period.

- Most firms do not plan to provide more up-to-date data than what was on the latest annual benefit statement or Statutory Money Purchase (SMP) illustration.

Since the fieldwork was conducted in autumn 2024, the following actions have now taken place to further support firms:

- The programme has published guidance on many aspects of the connection process and the first version of the approved dashboards standards have been published.

- All organisations who have expressed an interest in building a direct connection to the pension’s dashboards ecosystem have begun the process and the first organisations have successfully completed the technical connection process.

- A town hall event was held in December 2024 where pensions industry stakeholders had an opportunity to hear about progress and ask questions with speakers from the Money and Pensions Service (MaPS), the Department for Work and Pensions (DWP), The Pensions Regulator (TPR), the Financial Conduct Authority (FCA), GOV.UK One Login and industry. This included reflections on the connection experience as well as progress with the MoneyHelper Pensions Dashboard and plans for citizen testing.

1. Research background

1.1 Research background

1.1.1 Industry context

Pensions dashboards will provide individuals with a comprehensive view of their pension information, including their State Pension, all in one easily accessible online location. All pension schemes and providers within scope (in broad terms all personal pensions and all occupational pension schemes with at least 100 active and deferred members) are legally obligated to connect to the pensions dashboards ecosystem and be prepared to respond to requests for pension information by a final deadline of 31 October 2026. The Department for Work and Pensions (DWP) has introduced a staged connection approach set out in guidance.

This research focusses on personal and stakeholder pensions operated by FCA regulated pension providers only; occupational pension scheme trustees are regulated by The Pensions Regulator (TPR) who have carried out a similar survey. The findings from this survey, therefore, represent only part of the overall picture of pensions schemes and providers’ positions on connection to pensions dashboards. Large firms, which for the purposes of this research are defined as those pension providers with 5,000 or more relevant members, have a ‘connect by’ date in DWP’s guidance of 30 April 2025. Small firms, those with less than 5,000 relevant members, have a ‘connect by’ date in DWP’s guidance of 31 January 2026.

1.1.2 Research aims

The Money and Pensions Service (MaPS) commissioned Ipsos to conduct an online survey of Financial Conduct Authority (FCA) regulated pension providers to help the Pensions Dashboards Programme (PDP) understand how these firms are preparing to meet their dashboards obligations and how ready they are to meet their ‘connect by’ date in the DWP guidance.

The research had three core aims to explore:

- How well firms are prepared for the connection to the pensions dashboards central digital architecture.

- What specific barriers firms encountered in their preparation for pensions dashboards.

- If there were any key differences, in both level of preparation and the barriers faced, between different types of firms.

1.2 Research methodology

1.2.1 Sample

For the purposes of undertaking this research, FCA shared with MaPS the details of firms in scope of FCA’s pensions dashboard rules and an indication of their likely ‘connect by’ dates. This information was used by Ipsos to carry out the research study. Out of an initial pool of 136 firms, the final usable sample consisted of 130 firms, after cleaning out unusable contact information and removing firms who had opted out of the research.

1.2.2 Fieldwork

Fieldwork was conducted between 9 October 2024 and 6 November 2024. Initial email invitations were sent to 130 firms, followed by four reminder emails sent between 16 October 2024 and 4 November 2024. To maximise the response rate and ensure that those answering the survey were best placed to accurately answer all questions on behalf of their firm, all initial contacts were encouraged to forward the invitation to a more appropriate colleague if needed. Additionally, a PDF version of the questionnaire was attached to reminder emails to enable firms to collaborate on their answers within the organisation before inputting their responses online.

1.2.3 Response rates

In total 60 firms responded to the survey, resulting in a response rate of 46%. Larger firms (those administering 5,000 or more pension pots) had a much higher response rate (62%) than small firms (those administering less than 5,000 pension pots) (33%).

1.3 Interpreting the data in the report

Descriptive analysis was conducted on the survey data to report on the number and percentage of firms providing responses for each option in the questionnaire (see appendix). The percentages given in this report should be interpreted with caution and not be considered statistically representative of the wider industry sector. It is not possible to accurately calculate the non-response bias for large and small firms. It is therefore important to note that when the phrase ‘firms’ is used in the report, it is referencing those firms that responded to the survey rather than all FCA regulated firms in scope of dashboard duties. This is particularly the case for subgroup comparisons between large and small firms, noting that the base size for small firms is n=17. Throughout the report where the numbers of firms giving a particular response is less than 10, actual numbers of firms have been used rather than percentages.

Throughout the report comparisons of small and large firms are based on self-reported data given by firms in response to question (A3a) How many pension pots/plans have you identified? Large firms are those administering 5,000 or more pension pots and small firms are those administering less than 5,000 pension pots.

Back to top2. Firm profiles

2.1 Number and types of pensions administered

2.1.1 Number of pension pots administered

Overall, around 7 in 10 (71%) firms that responded to the survey self-reported as administering 5,000 or more pension pots (Figure 2.1). Of these ‘large’ firms, 6 in 10 (60%) reported administering between 5,000 and 99,999 pots, whilst 21% (9 firms) reported administering between 100,000 and 499,999 pots and a further 19% (8 firms) reported administering 500,000 or more. Only 17 firms reported being small firms, administering fewer than 5,000 relevant pots, amounting to 28% of those that completed the survey.

Figure 2.1 Number of pension pots/plans firms administered

(A3a) How many pension pots/plans have you identified?

Bases: All firms (60)

| Number of pension pots/plans firms administered | Firms (%) |

|---|---|

| Fewer than 5,000 | 28% |

| 5,000 to 99,999 | 43% |

| 100,000 to 499,999 | 15% |

| 500,000 or more | 13% |

2.1.2 Types of pensions administered

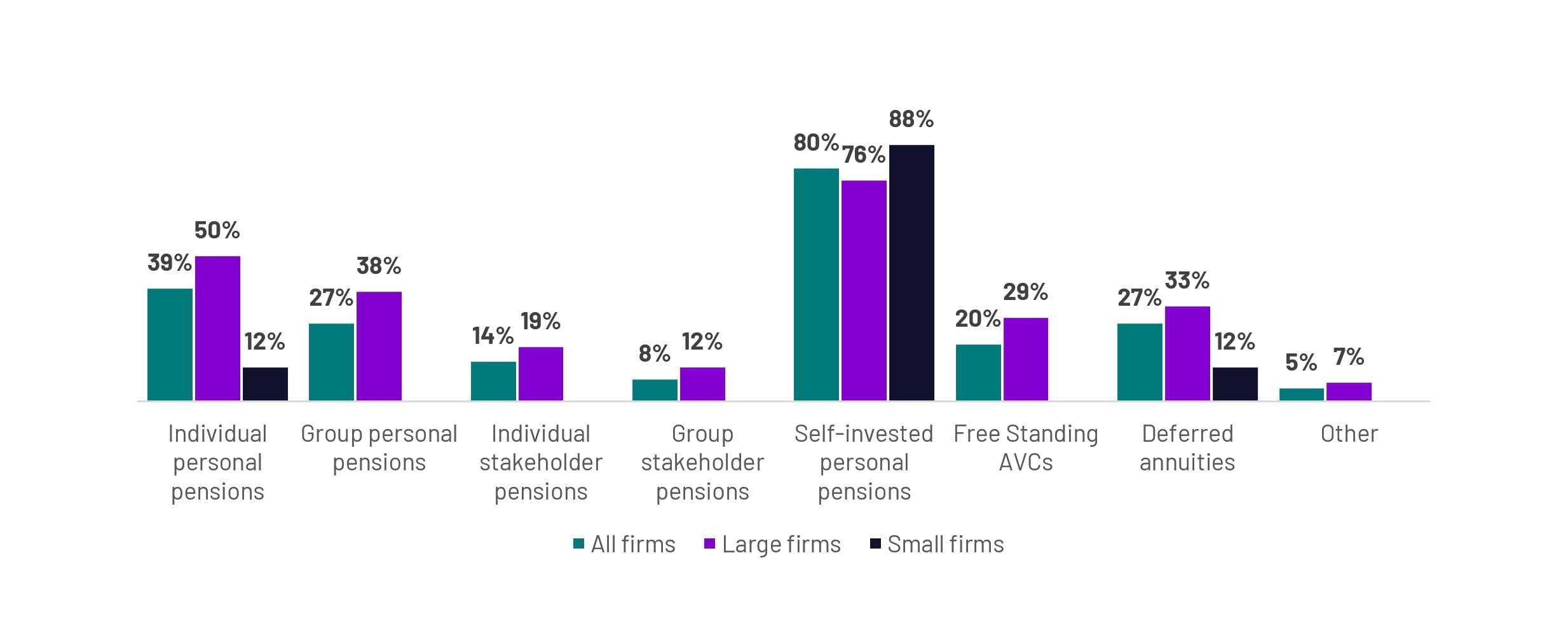

The most commonly administered type of pensions were self-invested personal pensions, which 4 in 5 firms (80%) reported administering (Figure 2.2). This was followed by individual personal pensions (39%), group personal pensions and deferred annuities (both 27%), and then free standing Additional Voluntary Contributions (AVCs) (20%). Eight firms (14%) reported administering individual stakeholder pensions, whilst 5 (8%) reported administering group stakeholder pensions. Three firms (5%) reported administering ‘other’ relevant types of pensions, which included: ‘Occupational Master Trust’, ‘TPA services for schemes (occupational registered pension schemes) including buy in’, and 'Trustee Investment Plans & Executive Personal Pension Plans'.

There were some clear differences in the types of pensions administered by small and large firms. Small firms only reported administering 3 pension types, and a large majority (88%) reported that they administered self-invested personal pensions (88%). Two small firms (12%) reported administering individual personal pensions, whilst a further 2 reported that they administered deferred annuities. Large firms most commonly administered the same 3 categories of pensions as small firms with self-invested personal pensions being administered by 3 in 4 (76%) large firms, individual personal pension administered by half (50%), and deferred annuities being administered by 1 in 3 (33%). However, every type of pension was administered by at least some large firms (Figure 2.2).

Figure 2.2 Types of pensions administered by firms

(A3b) What type(s) of pensions do you administer that are within the scope of FCA's final rules in PS 22/12

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| Pension types | All firms (%) | Large firms (%) | Small firms (%) |

|---|---|---|---|

| Individual personal pensions | 39% | 50% | 12% |

| Group personal pensions | 27% | 38% | 0% |

| Individual stakeholder pensions | 14% | 19% | 0% |

| Group stakeholder pensions | 8% | 12% | 0% |

| Self-invested personal pensions | 80% | 76% | 88% |

| Free standing AVCs | 20% | 29% | 0% |

| Deferred annuities | 27% | 33% | 12% |

| Other | 5% | 7% | 0% |

2.1.3 Number of different pension types administered

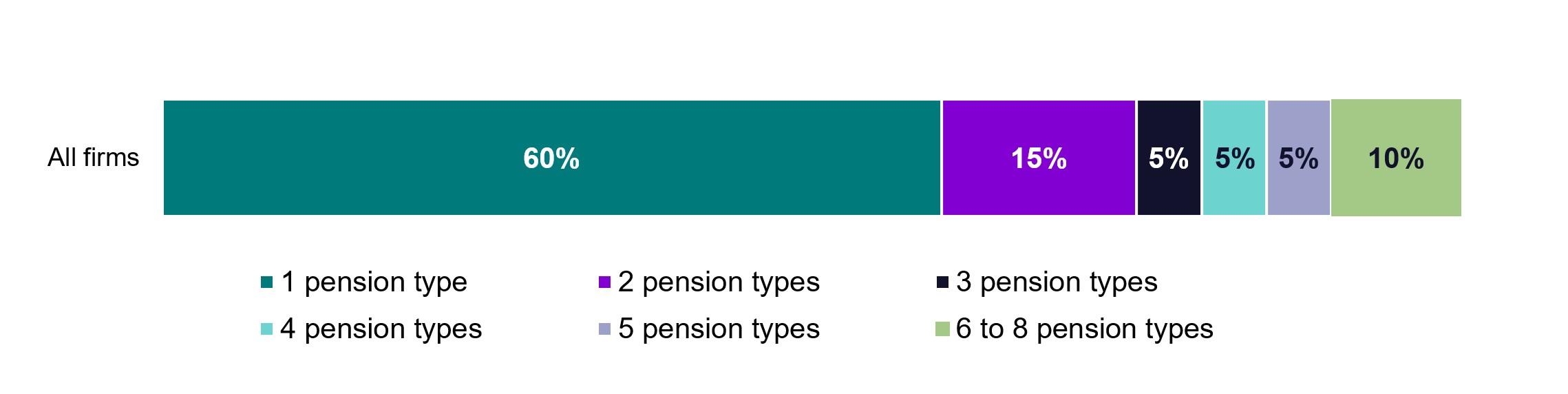

Overall, 6 in 10 firms (60%) only administered one type of pension (Figure 2.3). Of those firms that administered one pension type, 83% administered self-invested personal pensions. Two firms administered only individual personal pensions, whilst a further 3 administered only deferred annuities. Nine firms (15%) reported administering 2 types of pensions, whilst 25% reported administering between 3 and 8 types of pensions.

Figure 2.3 Number of different pension types that firms administer

(A3b) What type(s) of pensions do you administer that are within the scope of FCA's final rules in PS 22/12?

Bases: All firms (60)

| Number of pension types that firms administer | Firms (%) |

|---|---|

| 1 pension type | 60% |

| 2 pension types | 15% |

| 3 pension types | 5% |

| 4 pension types | 5% |

| 5 pension types | 5% |

| 6 to 8 pension types | 10% |

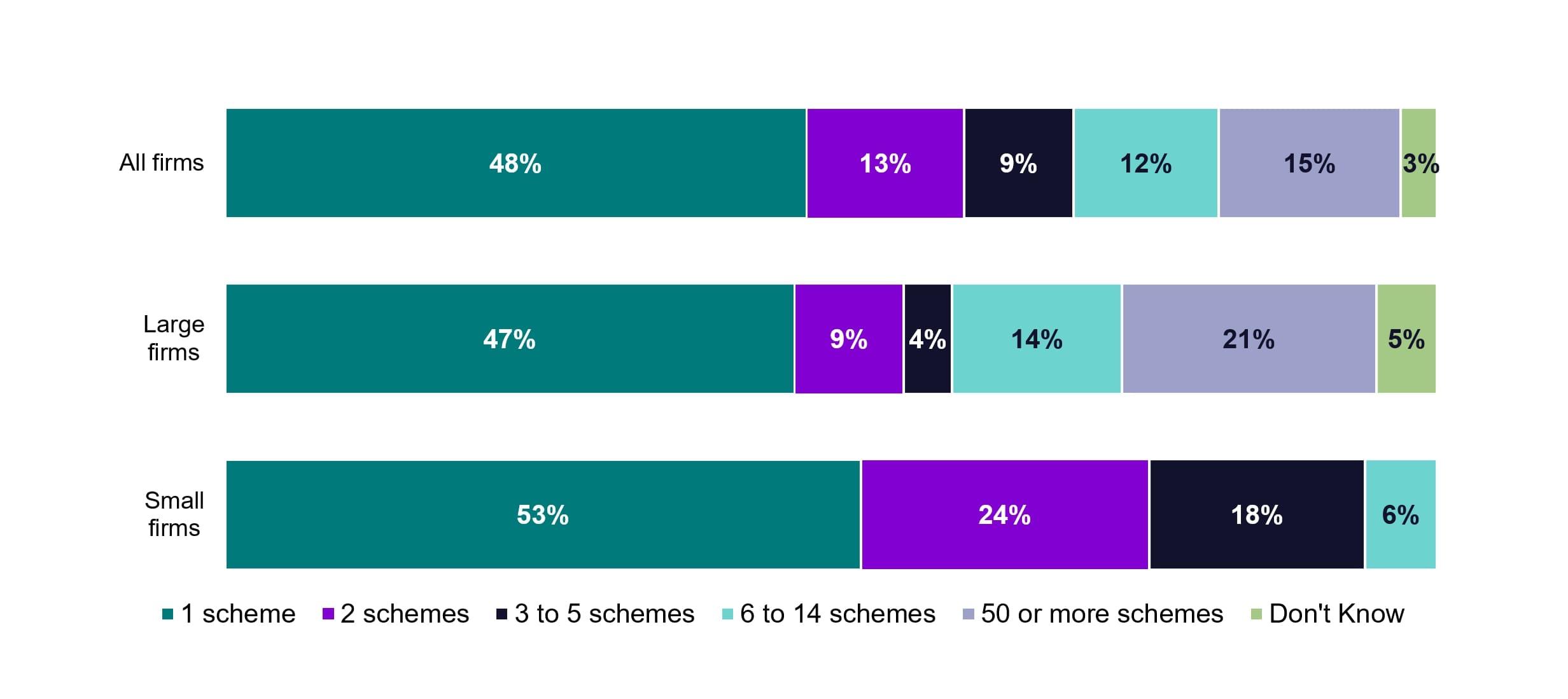

2.1.4 Number of schemes to connect

Almost half of all firms (48%) reported they would only be required to connect one scheme to the pensions dashboards central digital architecture (Figure 2.4). Three in 10 firms (34%) reported they needed to connect between 2 and 14 schemes. Only 9 large firms reported that they needed to connect more than 50 schemes (21%). Small firms tended to need to connect fewer schemes than larger firms, and three quarters of small firms (77%) reported they needed to connect 1 or 2 schemes. Three small firms reported needing to connect between 3 and 5 schemes, whilst only 1 small firm reported between 6 and 14 schemes.

Figure 2.4 Number of schemes firms intend to connect to the pensions dashboards central digital architecture

(A5) How many separate pension schemes will your firm be required to connect to the pensions dashboards central digital architecture?

Bases: All firms (60), Large firms (43), Small firms (17 *) * NB: Small base size

| Number of schemes | All firms | Large firms | Small firms |

|---|---|---|---|

| 1 scheme | 48% | 47% | 53% |

| 2 schemes | 13% | 9% | 24% |

| 3 to 5 schemes | 9% | 4% | 18% |

| 6 to 14 schemes | 12% | 14% | 6% |

| 50 or more schemes | 15% | 21% | 0% |

| Don’t know | 3% | 5% | 0% |

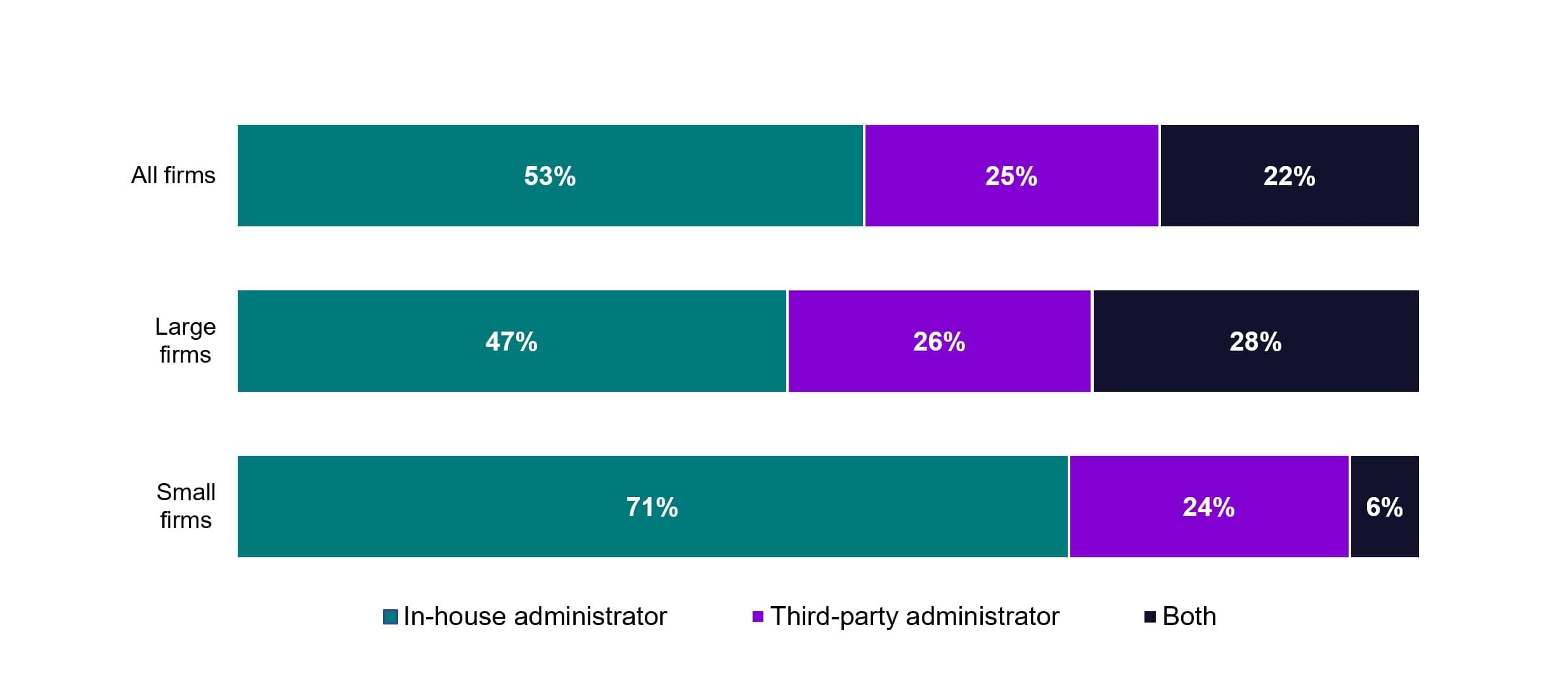

2.1.5 Type of administrator used

Around half of all firms reported using only an in-house administrator (53%), with a further 22% using an in-house administrator combined with a third-party administrator (Figure 2.5). A quarter of firms (25%) reported using only a third-party administrator. Small firms were more likely to use only an in-house administrator; (71%) compared to large firms (47%). Small firms were also much less likely to use a combination of in-house and third-party administrators, with only 1 small firm doing so compared to more than a quarter (28%) of large firms.

Figure 2.5 Types of administrators that firms use

(A4) Does the firm use an in-house administrator, third-party administrator or both?

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| Types of administrators | All firms | Large firms | Small firms |

|---|---|---|---|

| In-house administrator | 53% | 47% | 71% |

| Third-party administrator | 25% | 26% | 24% |

| Both | 22% | 28% | 6% |

2.2 How firms currently provide members with information

2.2.1 Existing methods of information provision

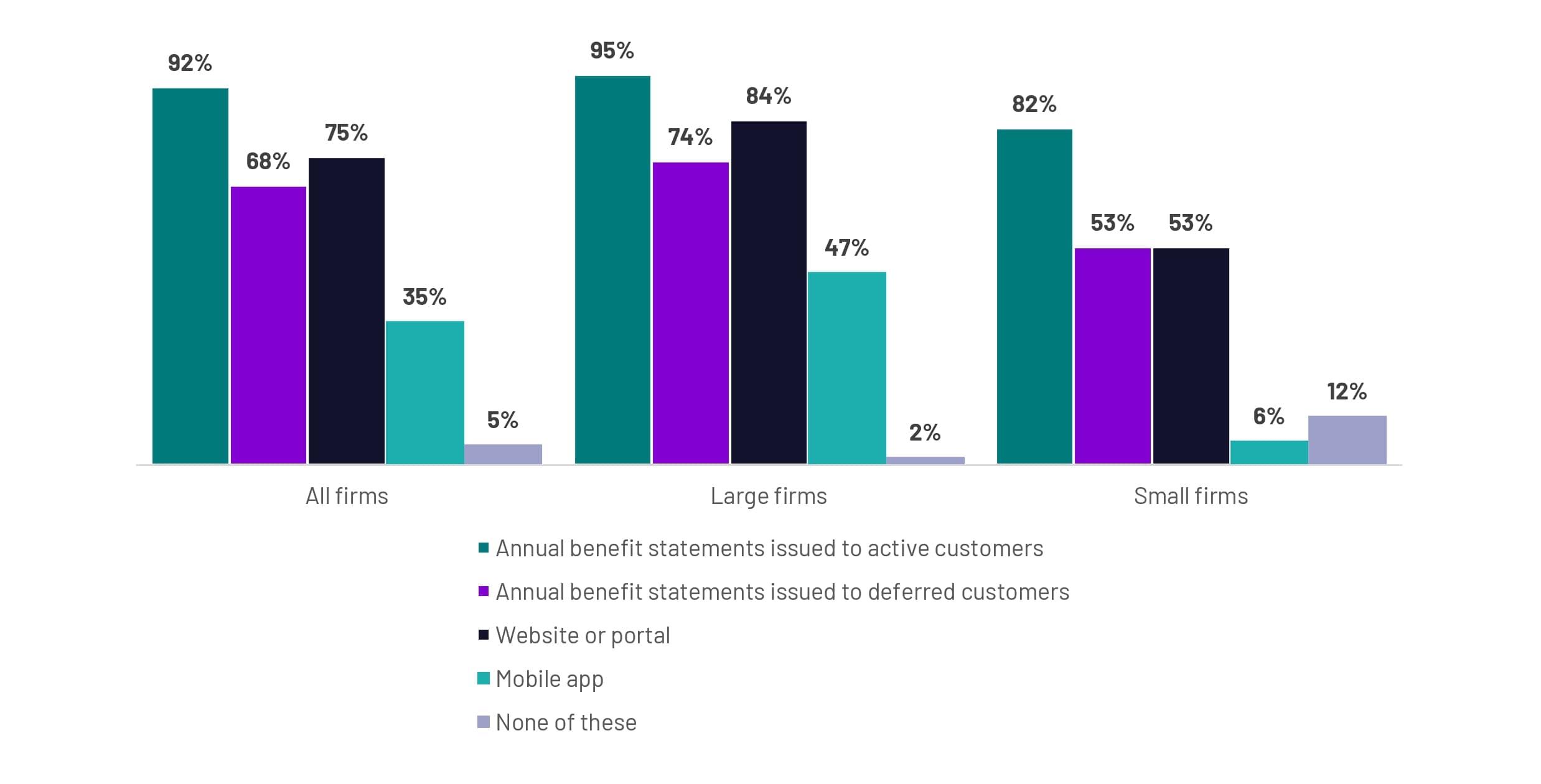

Firms were asked about the ways they currently provide their customers with information about the value of their pensions. Overall, 9 in 10 (92%) reported that they issue annual benefits statements to active customers, whilst around 2 in 3 (68%) reported that they issue annual benefit statements to deferred customers (Figure 2.6). Three in 4 (75%) reported providing value information via a website or portal for their customers, whilst 1 in 3 (35%) provide information via a mobile app.

Figure 2.6 How firms currently provide members with information on the value of their pensions

(A6) By which of the following methods do you currently provide members with information about the value of their pensions?

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Annual benefit statements issued to active customers | 92% | 95% | 82% |

| Annual benefit statements issued to deferred customers | 68% | 74% | 53% |

| Website or portal | 75% | 84% | 53% |

| Mobile app | 35% | 47% | 6% |

| None of these | 5% | 2% | 12% |

2.2.2 Portal, website or app usage

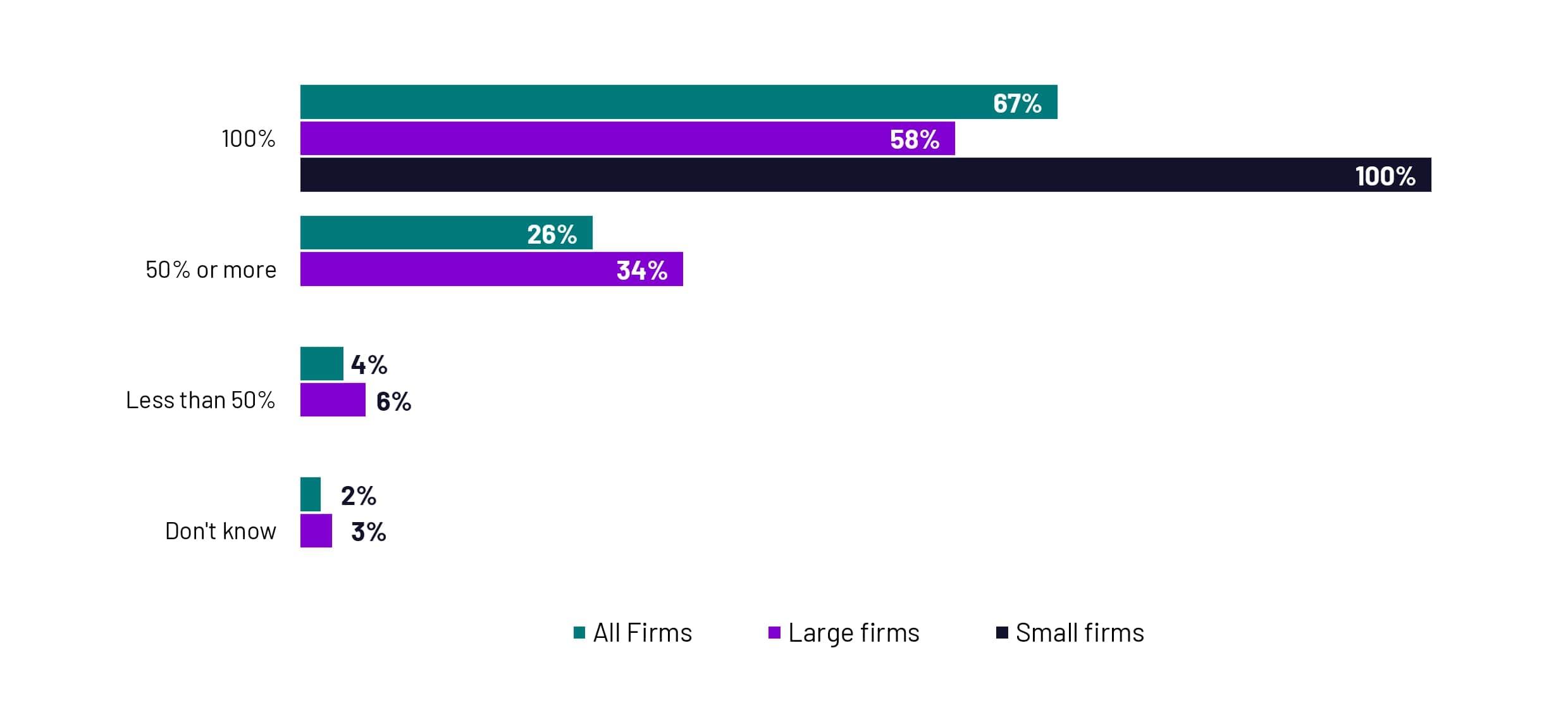

Firms that reported providing value information via a portal, website or mobile app were asked what proportion of their customers could access this information via these methods. Two in 3 of these firms (67%) reported that all of their customers could do this, while most others (22%) reported this applied to 75-99% of their customers (Figure 2.7). There was a notable difference in response by size of firm: 100% of small firms reported all of their customers could access value information in this way if they wished to do so, compared with 58% of large firms.

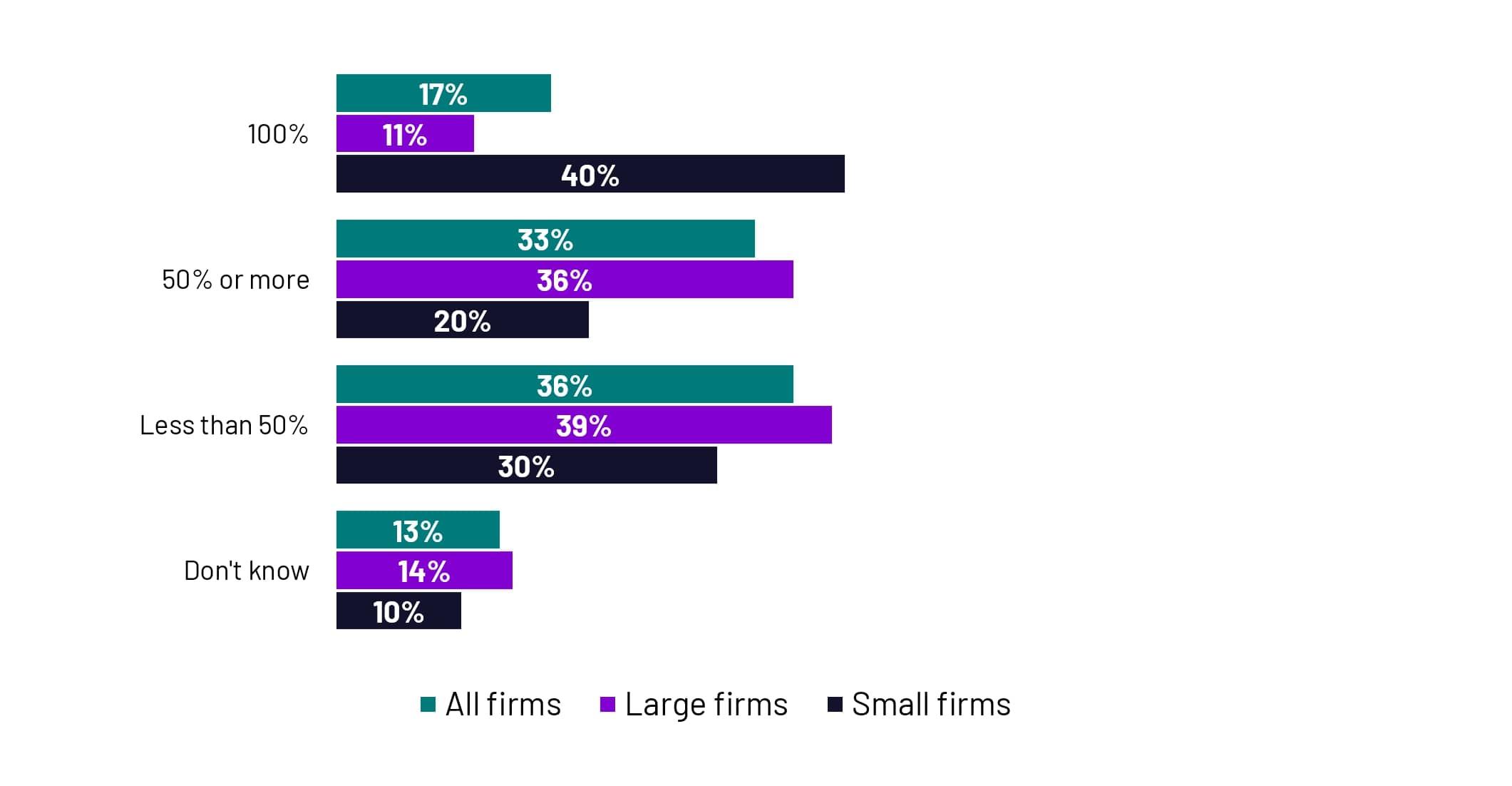

Firms that reported providing value information via a portal, website or mobile app were also asked what proportion of their customers had actually registered or enabled access to these services (Figure 2.8). Responses to this question were varied, but half of all firms (50%) reported that half or more of their customers had chosen to do this, and nearly 2 in 10 (17%) reported that this applied to all of their customers (Figure 2.7). Small firms were more likely to have reported that a higher proportion of their customers had done this, with 40% of small firms reporting all their customers had registered or enabled access to these services, compared to 11% of large firms.

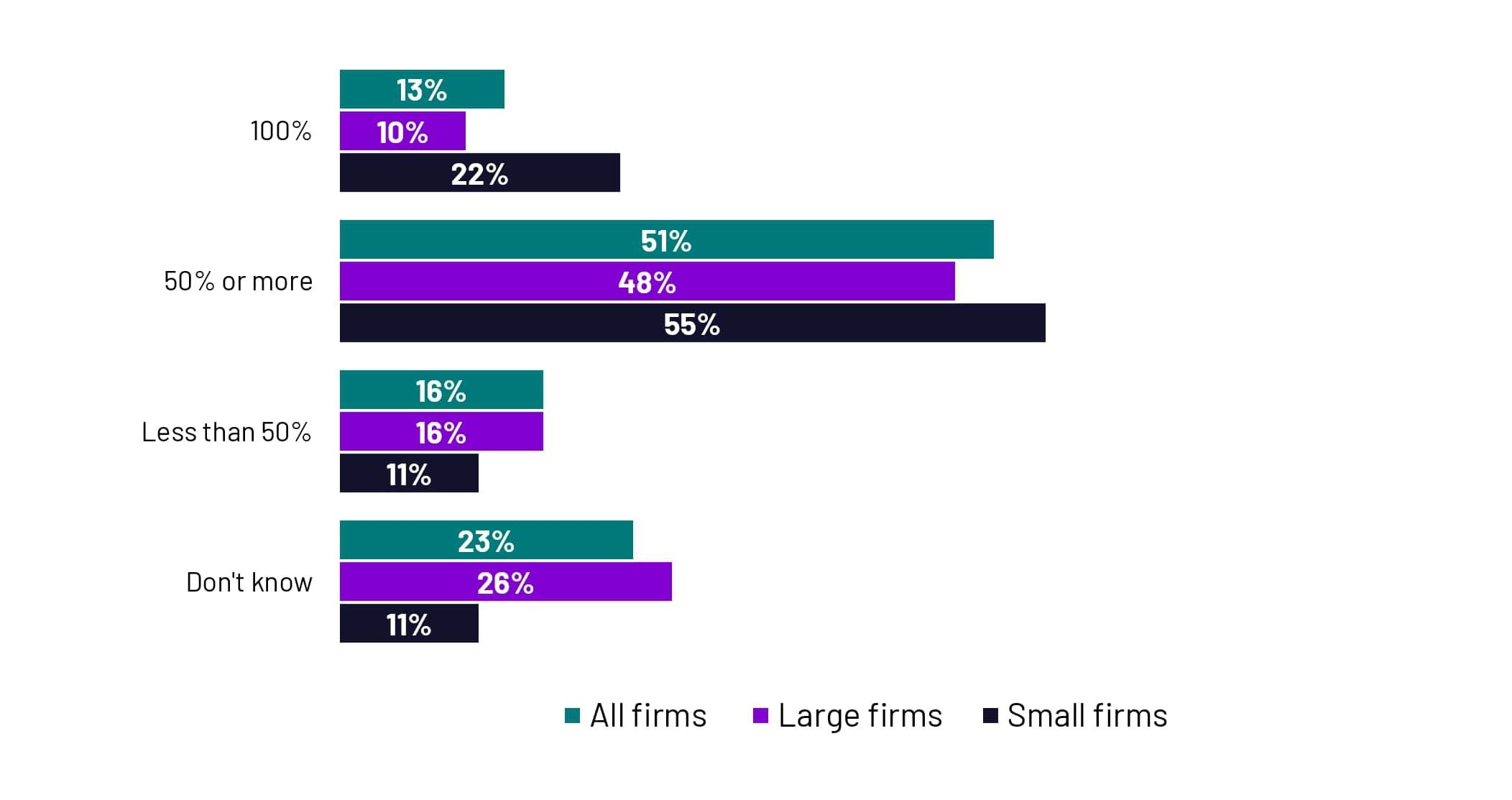

All firms where at least some customers had registered or enabled access to these services were asked what proportion of these customers had used them in the last 12 months (Figure 2.9). Again, responses were very varied but almost two-thirds of all firms (64%) reported that 50% or more of their customers had used these services, and around 1 in 10 (13%) reported that all of their customers had (Figure 2.8).

Figure 2.7 How firms currently provide members with information on the value of their pensions

(A7) Approximately what proportion of your customers could access their pensions value information via a portal, website or app, if they wish to do so (e.g. by registering)?

Bases: All able to utilise Website/Portal/App (46), Large firms (36), Small firms (10*) * NB: Small base

| All firms | Large firms | Small firms | |

|---|---|---|---|

| 100% | 67% | 58% | 100% |

| 50% or more | 26% | 34% | 0% |

| Less than 50% | 4% | 6% | 0% |

| Don’t know | 2% | 3% | 0% |

Figure 2.8 How many customers have registered or enabled access to website/portal/app services

(A8) Approximately what proportion of your customers have registered for or have enabled access to use these services?

Bases: All able to utilise Website/Portal/App (46), Large firms (36), Small firms (10*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| 100% | 17% | 11% | 40% |

| 50% or more | 33% | 36% | 20% |

| Less than 50% | 36% | 39% | 30% |

| Don’t know | 13% | 14% | 10% |

Figure 2.9 How many customers have used website/portal/app services in the last 12 months

(A9) Approximately what proportion of your customers that have registered for or have access to these services, have used any of them in the last 12 months?

Bases: All with more than 0% are registered for or have enabled access (40), Large firms (31), Small firms (9*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| 100% | 13% | 10% | 22% |

| 50% or more | 51% | 48% | 55% |

| Less than 50% | 16% | 16% | 11% |

| Don’t know | 23% | 26% | 11% |

Back to top

3. Engagement

3.1 Engagement with legislation, guidance and information

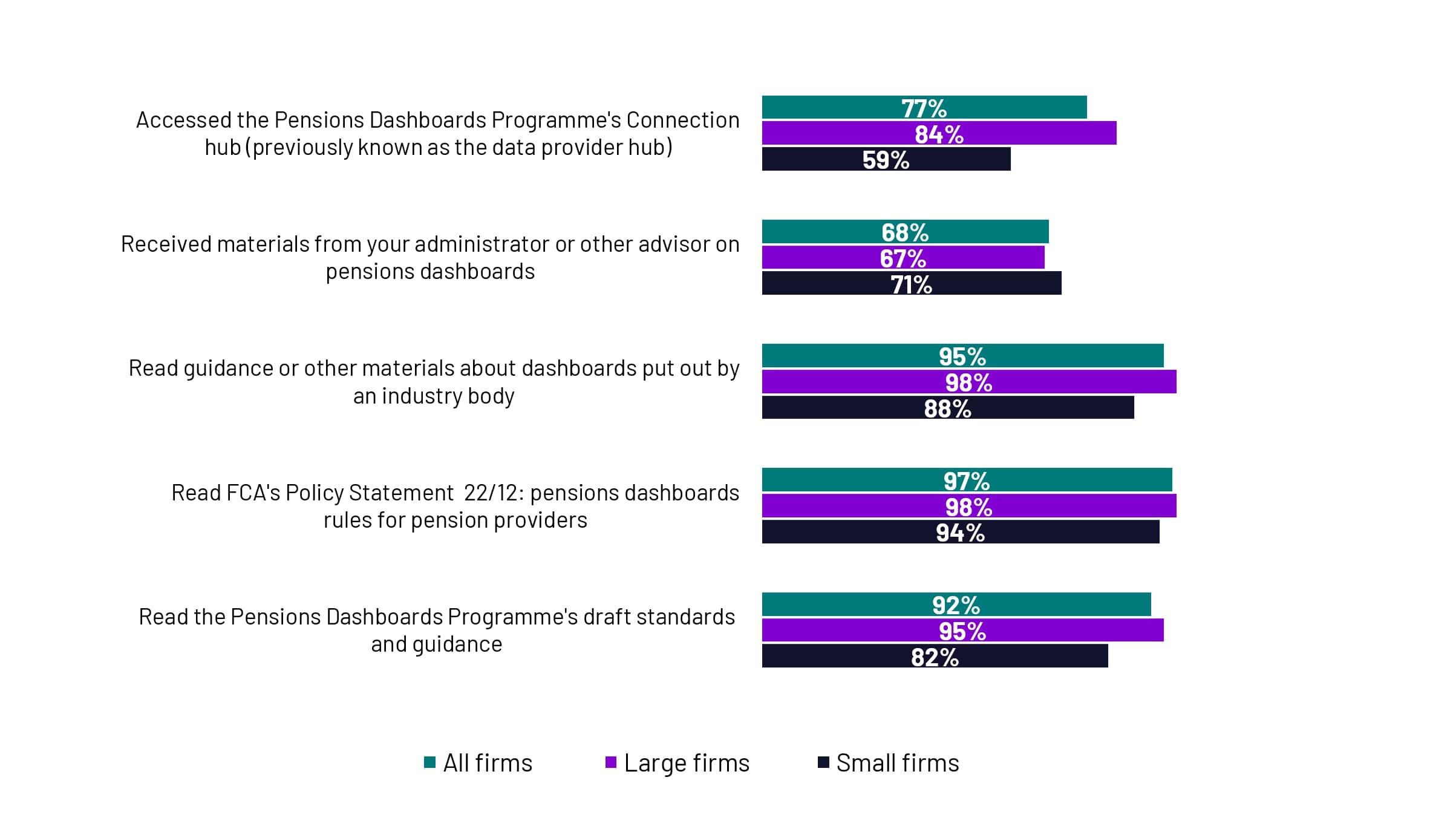

Firms’ engagement with legislation and guidance was generally very high. Nearly all firms (97%) reported that they had read the FCA’s Policy Statement 22/12: pensions dashboards rules for pensions providers, or read guidance or materials about dashboards put out by an industry body other than the PDP (95%), and over 9 in 10 (92%) had read the PDP’s draft standards and guidance (Figure 3.1). Fewer firms reported that they had accessed the PDP connection hub (77%), a resource intended primarily to assist firms that intend to connect directly and had received materials from their administrator or another advisor on pensions dashboards (68%). When comparing large and small firms, smaller firms were generally less likely to have engaged with all of these activities, and as expected were least likely to have accessed the PDP’s connection hub, with around 6 in 10 (59%) small firms reported to have done so compared to 84% of larger firms.

Figure 3.1 Firms’ preparations to ensure they are in line with guidance and duties

(E1) Have you, or the person/team accountable for making sure your firm is compliant with dashboard duties, done any of the following? Percentage of firms answering in the affirmative

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| Answer | All firms | Large firms | Small firms |

|---|---|---|---|

| Accessed the Pensions Dashboards Programme’s Connection hub (previously known as the data provider hub) | 77% | 84% | 59% |

| Received materials from your administrator or other advisor on pensions dashboards | 68% | 67% | 71% |

| Read guidance or other materials about dashboards put out by an industry body | 95% | 98% | 88% |

| Read FCA’s Policy Statement 22/12: pensions dashboards rules for pension providers | 97% | 98% | 94% |

| Read the Pensions Dashboards Programme’s draft standards and guidance | 92% | 95% | 82% |

3.2 Experience with the format of the standards and guidance on the PDP’s website

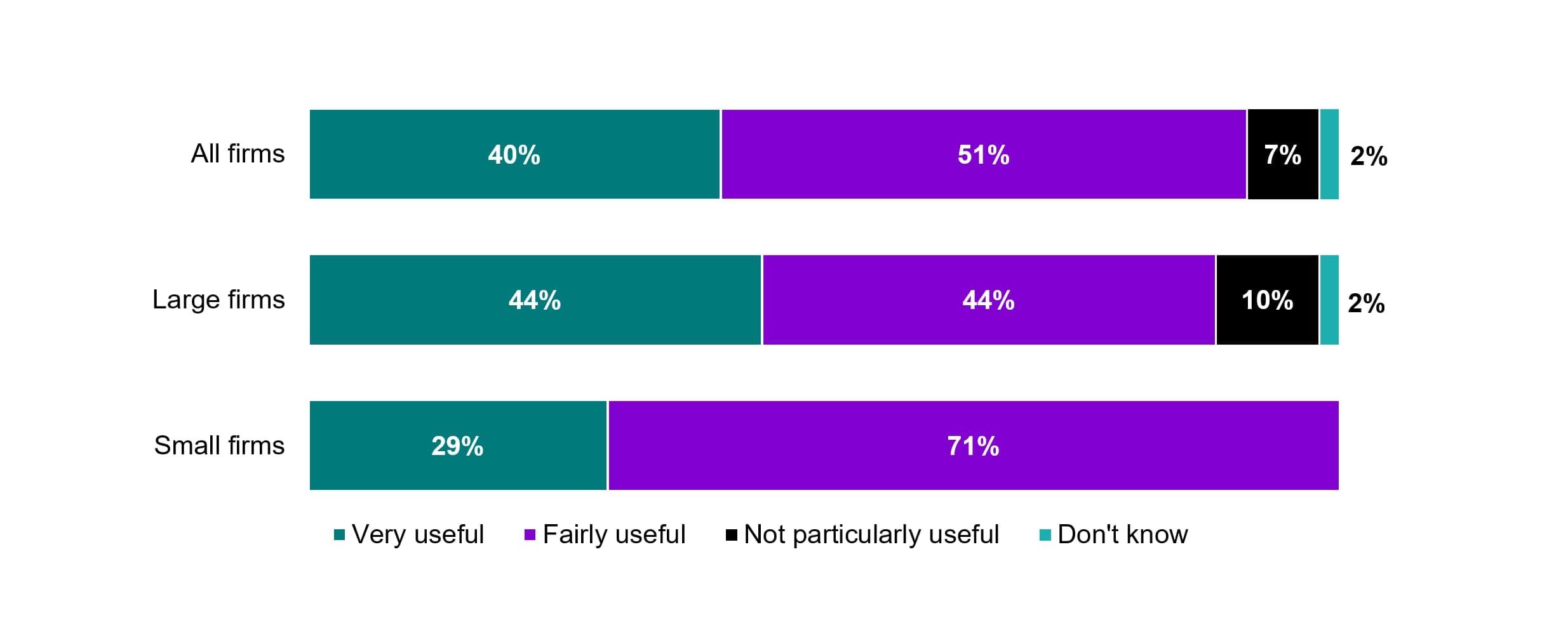

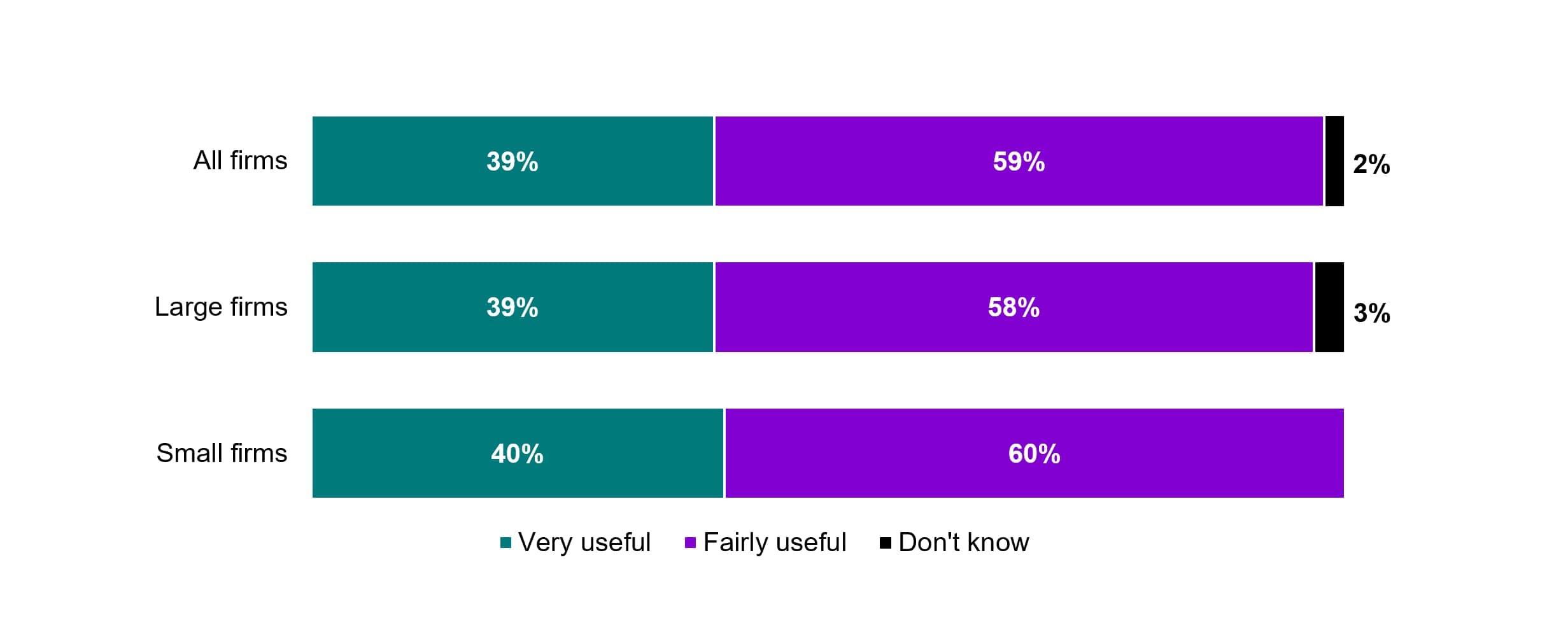

Firms who had read the draft standards and guidance on the PDP’s website, and those who had accessed the PDP connection hub, were asked how useful they found these resources. Firms who had read the guidance generally felt positive about its format, with 91% of firms reported they found the format of the draft standards and guidance either very or fairly useful (Figure 3.2). All firms who had accessed the connection hub reported that they found the information contained there at least ‘Fairly useful’. (Figure 3.3). Smaller firms were generally less positive about the format of the standards and guidance, with only 4 small firms (29%) feeling that the format was ‘Very useful’, compared to 44% of large firms. There were no clear differences between small and large firms’ experiences with the information contained on the connection hub.

Figure 3.2 Firms’ experience with the format of the draft standards and guidance on the PDP’s website

(E2) How useful did you or your team members find ...? a) The format of the draft standards and guidance on the Pensions Dashboards Programme's website

Bases: All who read the FCA's policy statement or the PDP draft standards and guidance (55), Large firms (41), Small firms (14)

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Very useful | 40% | 44% | 29% |

| Fairly useful | 51% | 44% | 71% |

| Not particularly useful | 7% | 10% | 0% |

| Not at all useful | 0% | 0% | 0% |

| Don’t know | 2% | 2% | 0% |

Figure 3.3 Firms’ experience with the information contained on the PDP connection hub

(E2) How useful did you or your team members find ...? b) The information provided on the Pensions Dashboards Programme's connection hub (previously known as the data provider hub)

Bases: All who have accessed information provided on the PDP connection hub (46), Large firms (36), Small firms (10*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Very useful | 39% | 39% | 40% |

| Fairly useful | 59% | 58% | 60% |

| Not particularly useful | 0% | 0% | 0% |

| Not at all useful | 0% | 0% | 0% |

| Don’t know | 2% | 3% | 0% |

3.3 Firms ‘connect by’ dates

3.3.1 DWP guidance

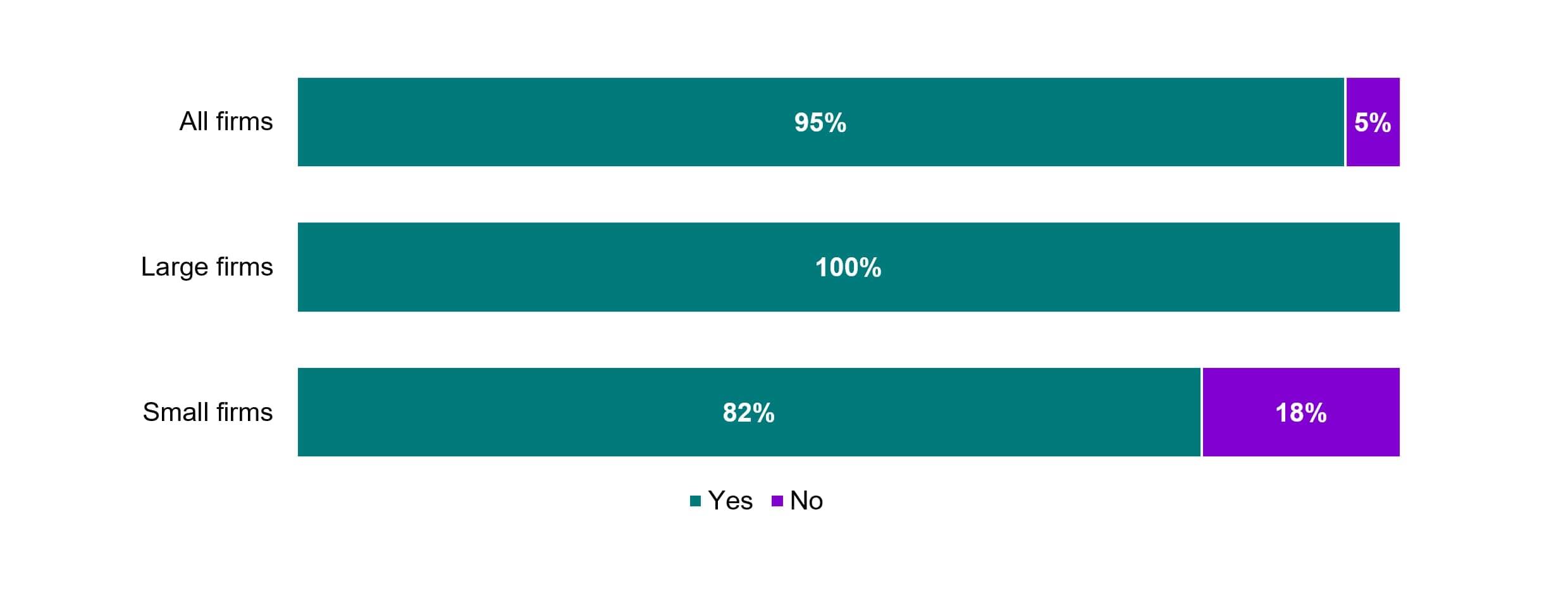

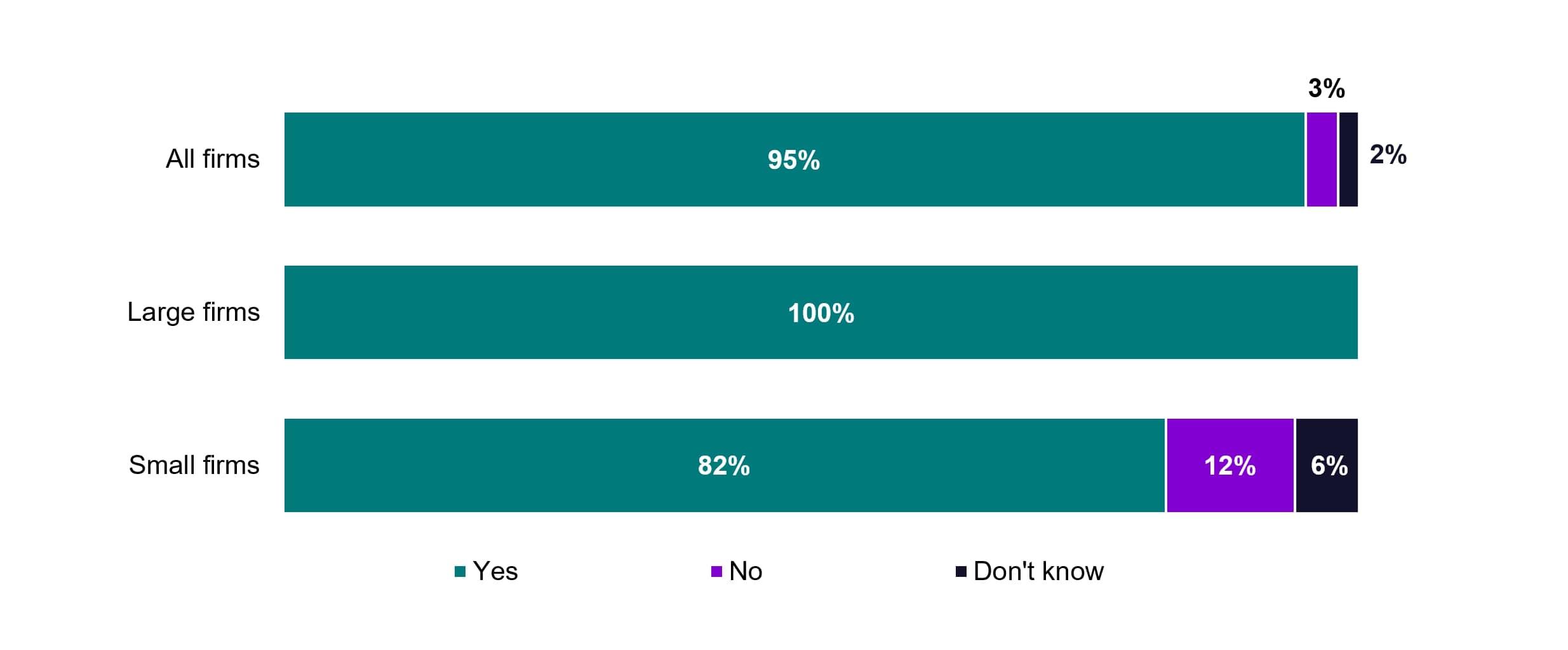

DWP guidance on connection sets out a staged timetable for connection to the pensions dashboards ecosystem and assigns firms dates to be connected by – 30 April 2025 for firms with 5,000 or more pots in accumulation, and 31 January 2026 for firms with fewer than 5,000 pots in accumulation. Overall, most firms (95%) reported having read the DWP guidance setting out the ‘connect by’ date for firms (Figure 3.4). Only 3 small firms reported that they had not read this guidance.

Figure 3.4 Percentage of firms that have read the DWP guidance setting out firms ‘connect by’ dates

(C1) Have you read this guidance?

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Yes - has read guidance | 95% | 100% | 82% |

| No - had not read guidance | 5% | 0% | 18% |

| Don’t know | 0% | 0% | 0% |

3.3.2 Awareness of ‘connect by’ date

Most firms (95%) reported being aware of their ‘connect by’ date. Again, the only firms that reported not knowing this date were 3 small firms (18%) (Figure 3.5).

Figure 3.5 Firms’ awareness of ‘connect by’ date

(C2) Do you know the 'connect by' date for your firm?

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Yes - knows 'connect by' date | 95% | 100% | 82% |

| No - does not know 'connect by' date | 3% | 0% | 12% |

| Don’t know | 2% | 0% | 6% |

When asked to input their ‘connect by’ dates, almost all large firms (98%) reported this accurately, as April 2025. However, of the 14 small firms that said they knew their ‘connect by’ date 9 (64%), gave an incorrect date when asked what this was. These firms gave a wide variety of incorrect dates. Six small firms gave an earlier date than their actual ‘connect by’ date, with the most common being April 2025 (the date for large firms), given by 3 small firms. Of the small firms that incorrectly gave a later date than their actual ‘connect by’ date, the most common was October 2026 (the final deadline), which was given by 2 small firms. No firms believed they had a date later than the final deadline of 31 October 2026.

Back to top4. ‘Connect by’ dates

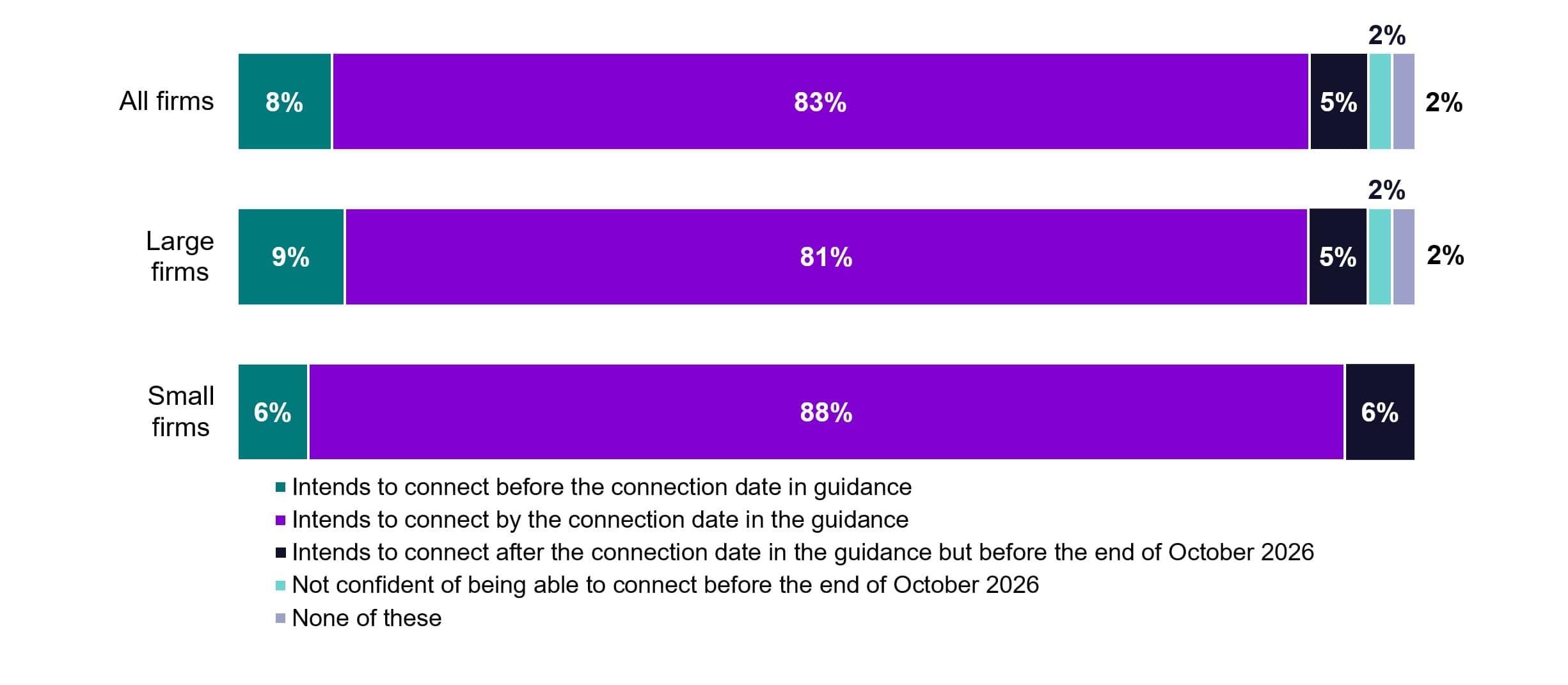

4.1 Intention to connect by ‘connect by’ date

Overall, 9 in 10 firms (91%) intended to connect either before or by their ‘connect by’ date, with only 1 firm not being confident they would be able to connect by the final deadline of 31 October 2026 (Figure 4.1). Firms answered this question based on their understanding of their connect by date. The intentions of small and large firms were very similar here but given the fact that a large proportion of small firms stated the wrong connect by date, the number of small firms intending to connect earlier or later than their given ‘connect by’ date (only 1 firm in each case) is not reflective of the real position of these firms.

Figure 4.1 Percentage of firms that intend to connect before and after their ‘connect by’ dates.

(C4) Which of the following best describes your firm's position in respect of your ‘connect by’ date?

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Intends to connect before the connection date in guidance | 8% | 9% | 6% |

| Intends to connect by the connection date in the guidance | 83% | 81% | 88% |

| Intends to connect after the connection date in the guidance but before the end of October 2026 | 5% | 5% | 6% |

| Not confident of being able to connect before the end of October 2026 | 2% | 2% | 0% |

| None of these | 2% | 2% | 0% |

| Don’t know | 0% | 0% | 0% |

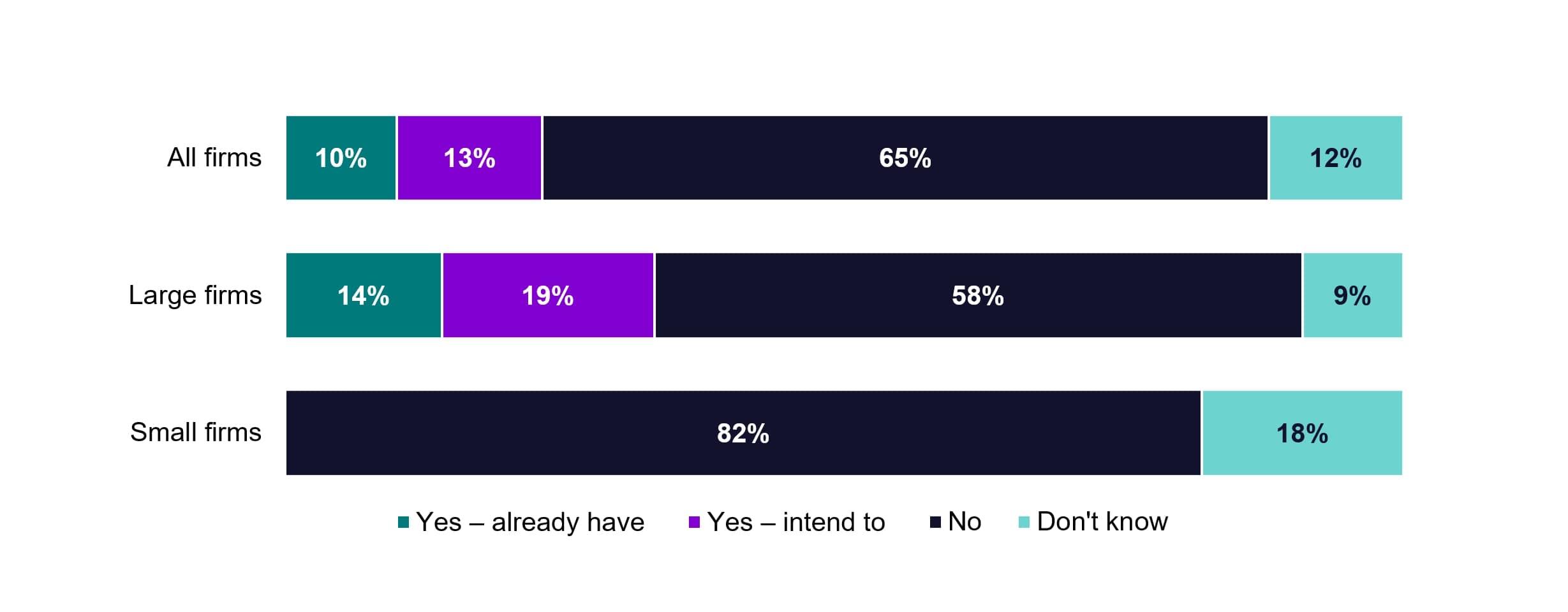

4.2 Firms’ intention to use the FCA’s modification by consent

The FCA’s modification by consent enables firms to connect in line with their ‘connect by’ date in guidance despite not being able at that point to comply with the legislative requirements for 100% of their relevant members. Around two-thirds (65%) of firms did not intend to make use of this (Figure 4.2). Nearly a quarter (23%) of firms had either already used or were intending to use modification by consent, these were all large firms, which aligns with large firms’ higher likelihood to be responsible for connecting multiple schemes. Seven firms (12%) did not know whether they would use modification by consent or not. Of those firms that did intend to use, or were already using, modification by consent, 71% expected to make 90-99% of their book available by their ‘connect by’ date. Almost all of the remaining firms (3) expected to make between 50-79% of their book available, whilst 1 firm reported that they didn’t know how much of their book would be available.

Figure 4.2 Do firms intended to use modification by consent

(C18) Does your firm intend to avail itself of the FCA's modification by consent?

Bases: All (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Yes – already have | 10% | 14% | 0% |

| Yes – intend to | 13% | 19% | 0% |

| No – does not intend to | 65% | 58% | 82% |

| Don’t know | 12% | 9% | 18% |

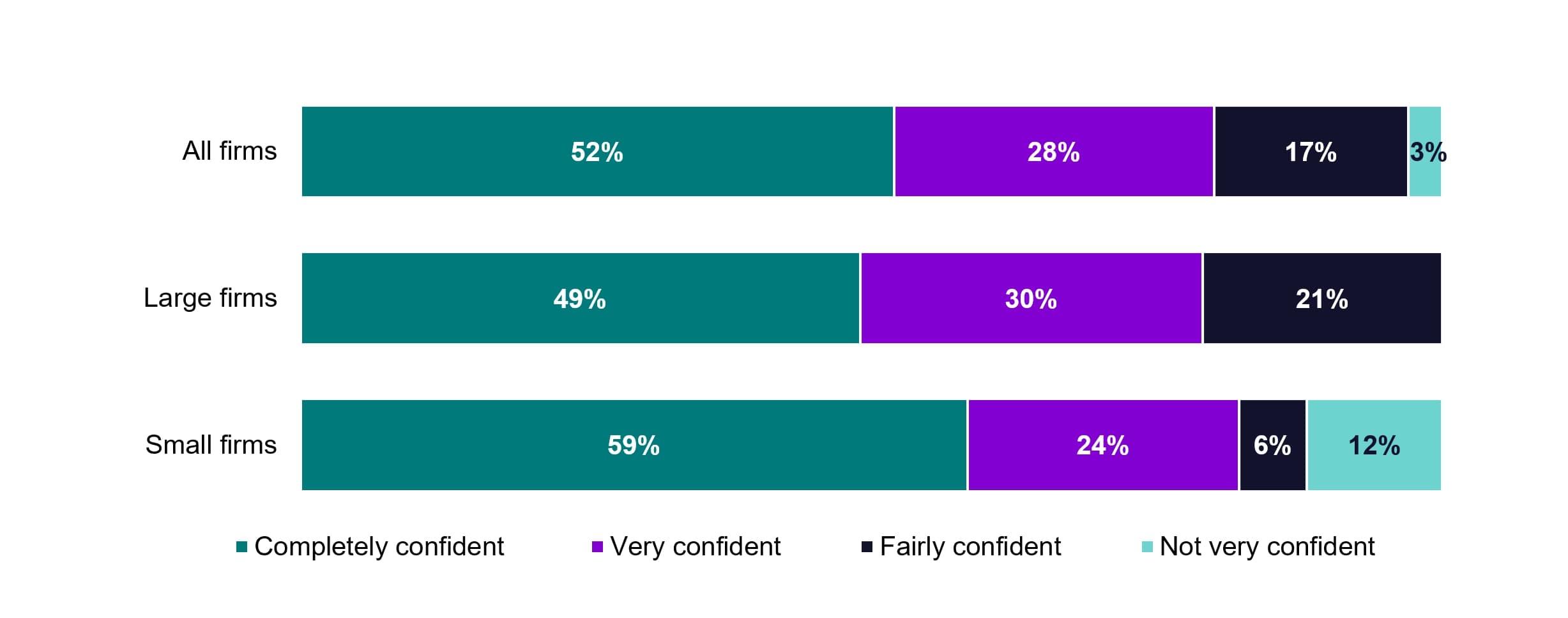

4.3 Confidence meeting ‘connect by’ dates

4.3.1 Degrees of confidence across requirements

Firms were asked how confident they were that they would be able to meet 3 key requirements for connection by their ‘connect by’ date. Firms chose between being ‘Completely confident’, ‘Very confident’, ‘Fairly confident’, ‘Not very confident’, ‘Not at all confident’ or ‘Don’t know’:

- Implementing their decisions on which personal and contact data items they would use for matching members to their records.

- Having fully digitised and accurate data for customer matching.

- Being able to provide timely, accurate and up-to-date value estimates for all pensions.

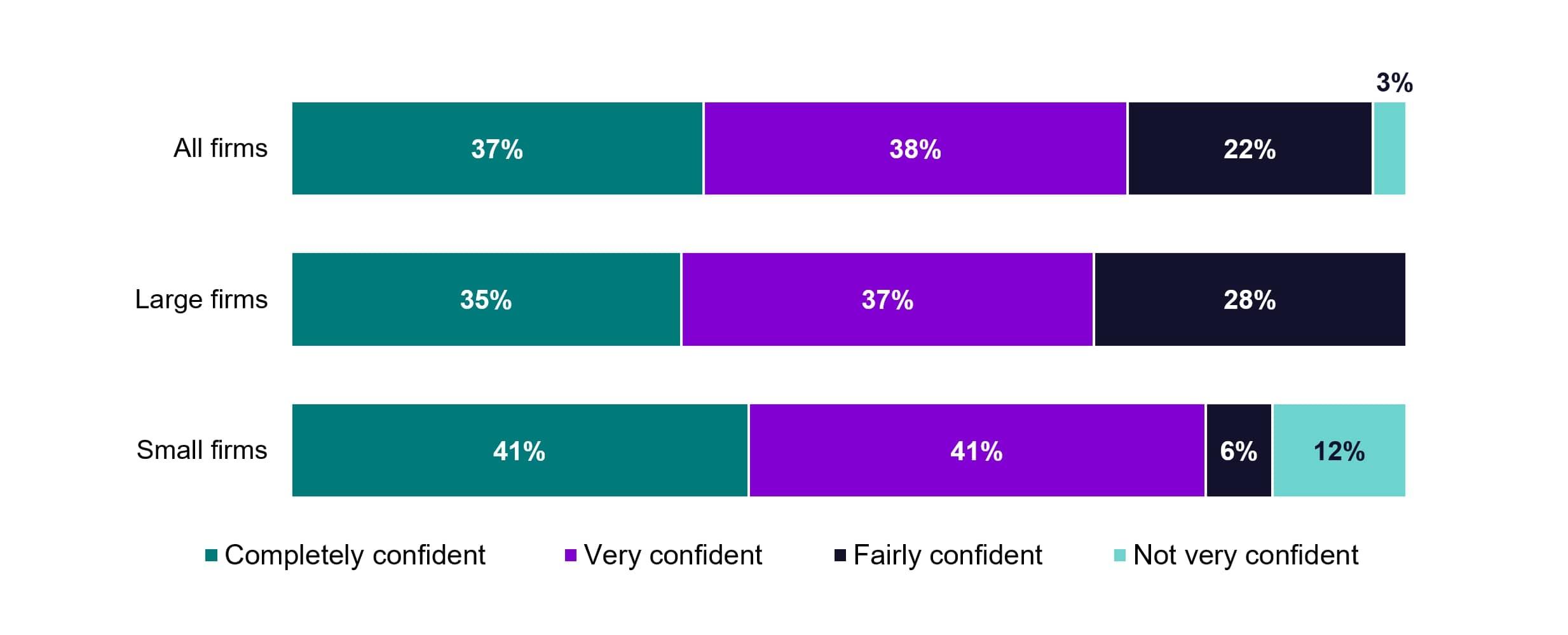

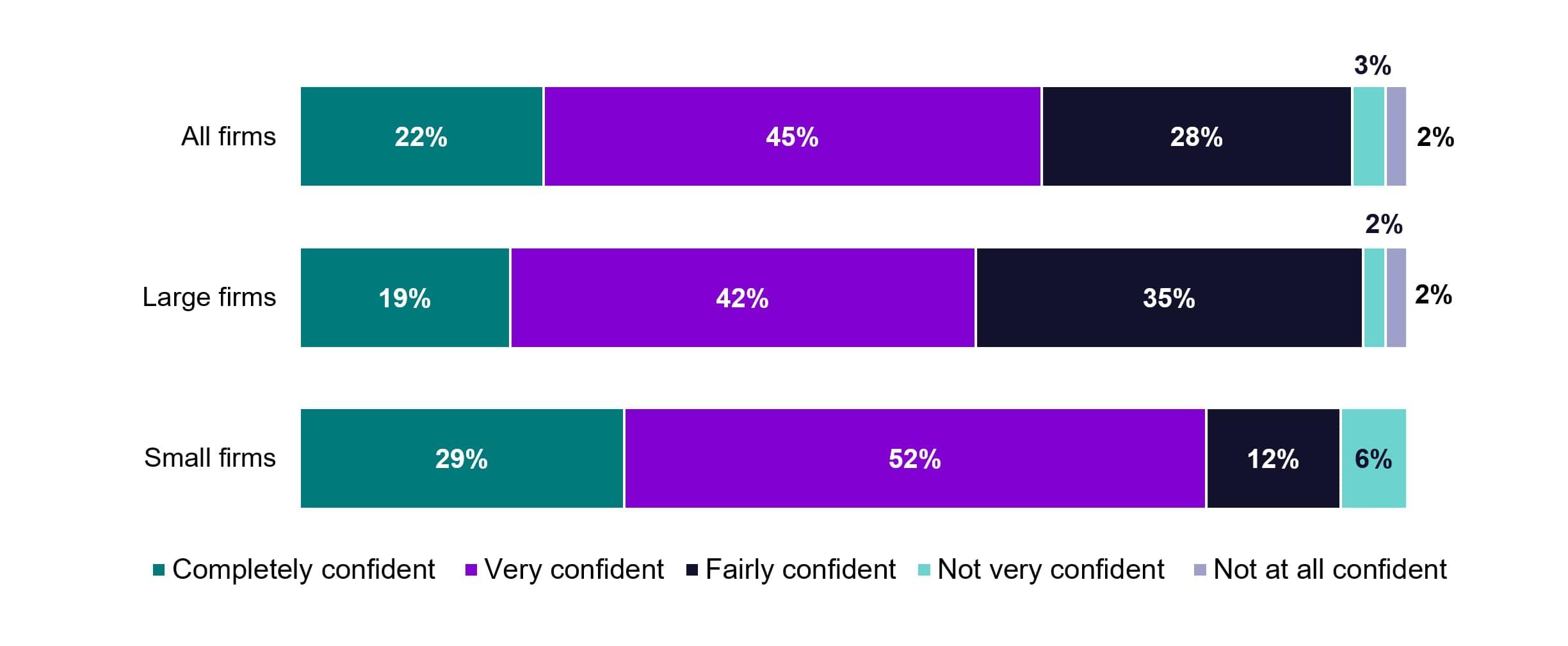

Firms were broadly confident in being able to meet all these requirements, and a large majority reported that they were at least ‘Very confident’ in being able to meet each requirement (Figure 4.3, 4.4, 4.5). Firms expressed the highest degree of confidence that they would have implemented their decisions on which personal and contact data items they would be using for matching members to their record (Figure 4.3). Over half (52%) of all firms reported that they were completely confident that they would have done this by the time of their ‘connect by’ date, with a further 28% stating that they were very confident they would have done so. Confidence was lower for having fully digitised and accurate data for record matching (Figure 4.4.), and around 4 in 10 firms (37%) reported that they were completely confident they would have done this, whilst a similar proportion reported they were very confident. By comparison, 2 in 10 firms (22%) were completely confident that they would be able to provide timely, accurate and sufficiently up-to-date value estimates for all pensions, though almost half (45%) felt very confident that they would be able to do this (Figure 4.5).

Small firms exhibited a higher diversity in confidence levels than larger firms. A higher proportion of small firms reported being completely or very confident across all categories (Figure 4.3, 4.4, 4,5).

Figure 4.3 Firms’ confidence in being able to implement decisions on data matching items

(C5) For each of the below statements, please confirm how confident you are that by the 'connect by' date for your firm you will...? (C5a) … have implemented your decisions on which personal and contact data items you will be using for matching members to their records

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Completely confident | 52% | 49% | 59% |

| Very confident | 28% | 30% | 24% |

| Fairy confident | 17% | 21% | 6% |

| Not very confident | 3% | 0% | 12% |

| Not at all confident | 0% | 0% | 0% |

| Don’t know | 0% | 0% | 0% |

Figure 4.4 Firms’ confidence in having fully digitised and accurate data for matching customer records

(C5b) … b) Have fully digitised and accurate data for matching customer records

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Completely confident | 37% | 35% | 41% |

| Very confident | 38% | 37% | 41% |

| Fairy confident | 22% | 28% | 6% |

| Not very confident | 3% | 0% | 12% |

| Not at all confident | 0% | 0% | 0% |

| Don’t know | 0% | 0% | 0% |

Figure 4.5 Firms’ confidence in being able to provide accurate and timely data

(C5c) … be able to provide timely, accurate and sufficiently up-to-date value estimates for all pensions

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Completely confident | 22% | 19% | 29% |

| Very confident | 45% | 42% | 52% |

| Fairy confident | 28% | 35% | 12% |

| Not very confident | 3% | 2% | 6% |

| Not at all confident | 2% | 2% | 0% |

| Don’t know | 0% | 0% | 0% |

4.3.2 Reasons for lack of confidence in being able to connect

Firms that reported they were less than ‘very confident’ that they would have fully digitised matching data, be able to provide accurate and up-to-date value estimates, or reported that they intended to connect after their ‘connect by’ date were asked to describe the main issues that resulted in a lower level of confidence. The 22 firms that answered this question gave diverse reasons for a lack of confidence. Several prominent themes, along with illustrative quotes, are given below.

Reliance on third-party suppliers/Co-ordinating multiple TPAs

Firms reported that reliance on a third-party supplier was a reason for a lower confidence in being able to connect by their ‘connect by’ date. The specific obstacles presented by using third party suppliers were varied but tended to focus on challenges with coordination and information sharing across organisations.

Our technology supplier is responsible for connection to the dashboard.

Small firm

Multiple TPA delivery plans to coordinate and general TPA capacity.

Large firm

Dependent on our system provider.

Small firm

Strategic development with our Outsourced partners involving data migrations currently in progress.

Small firm

Lack of internal capacity

Firms reported that internal capacity was an obstacle to high levels of confidence. This was generally due to competing priorities within the organisation and other projects being delivered concurrently

Resource stretch/data availability [...] at a time when the business is going through a significant data project.

Small firm

Resourcing and conflicting priorities due to business transformation projects ongoing.

Small firm

Lack of full testing

Firms reported that not having completed full testing was also an obstacle to high levels of confidence.

We have not undertaken testing as yet

Small firm

We are in the very early stages of testing with PDP, there are a lot of requirements and connection process details still to be confirmed

Small firm

5. How firms intend to connect

5.1 How firms intend to connect

5.1.1 Direct connection vs third-party supplier

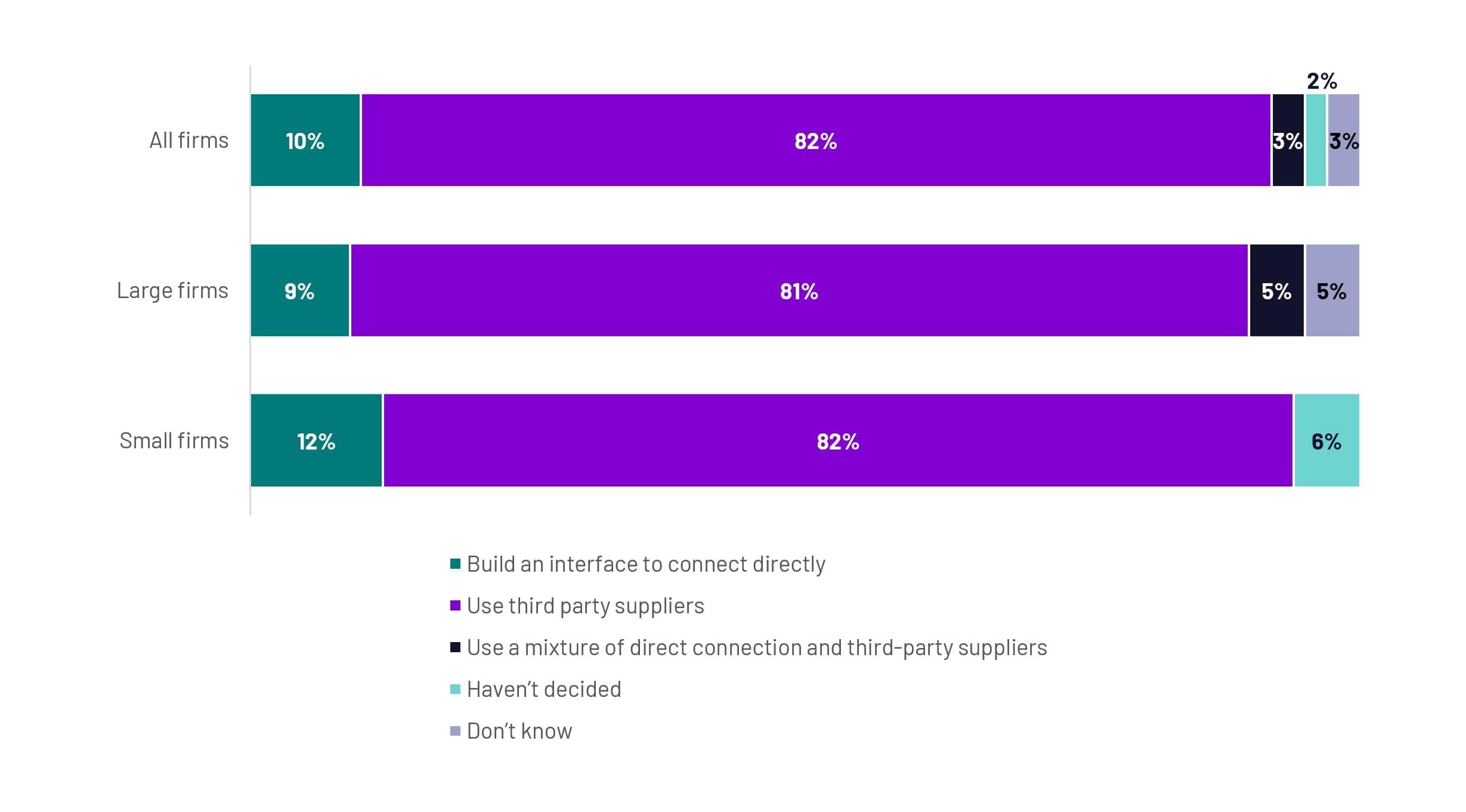

Four in 5 firms (82%) intended to connect to the central digital architecture via a third-party supplier, whilst 1 in 10 (10%) intended to connect directly by building their own interface (Figure 5.1).

Figure 5.1 Proportion of firms that intend to connect directly or use a third-party supplier

(C9) Which of the following best describes the way in which your firm intends to connect to the central digital architecture?

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Build an interface to connect directly | 10% | 9% | 12% |

| Use third-party suppliers | 82% | 81% | 82% |

| Use a mixture of direct connection and third-party suppliers | 3% | 5% | 0% |

| Haven’t decided | 2% | 0% | 6% |

| Don’t know | 3% | 5% | 0% |

5.1.2 Firms intending to connect via third-party supplier

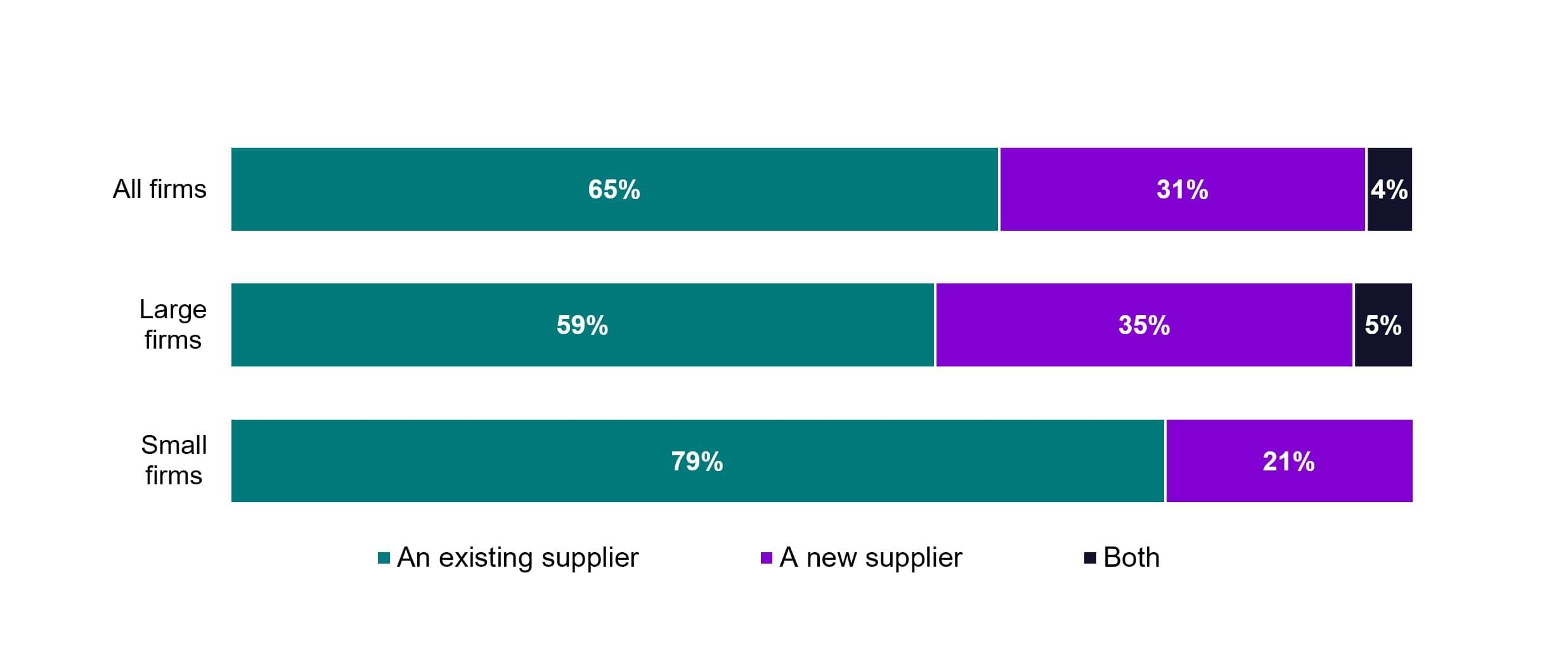

Overall, of those firms intending to use a third-party supplier to connect, nearly 2 in 3 (65%) reported that they would use an existing supplier (Figure 5.2). This was more pronounced for small firms, where 8 in 10 (79%) intended to use an existing supplier, compared with around 6 in 10 (59%) large firms. Intention to use a new supplier was higher for large firms (35%) than it was for small firms (21%), and only 3 large firms intended to use a mixture of both new and existing suppliers.

Of those firms that intended to use existing suppliers 23% reported that the process of amending contracts was already complete, with a further 54% reporting that the process was already underway. For those that reported the process was underway, more than 9 in 10 (95%) reported that this would be complete within 3 to 6 months. By contrast 17% of firms reported that they had not begun the process, and 2 small firms reported that they did not need to amend their contracts.

Of the 33 firms that reported they intended to use a new supplier, 61% reported that they had already completed the process of procuring them. All firms that had not already completed the procurement process expected to complete it within the next 3 to 6 months.

Figure 5.2 Proportion of firms that intend to use new and existing third-party suppliers

(C12) Thinking about the third-party supplier(s) that you will use to connect to the dashboard’s architecture, is this likely to be?

Bases: All who intend to use 3rd party suppliers (51), Large firms (37), Small firms (14*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| An existing supplier | 65% | 59% | 79% |

| A new supplier | 31% | 35% | 21% |

| Both | 4% | 5% | 0% |

| Don’t know | 0% | 0% | 0% |

5.1.3 Firms intending to connect directly

Of the 6 firms that intended to connect to the central digital architecture directly, 4 reported that they had already started the process of building an interface, whilst the remaining 2 reported that they planned to begin doing so in the next 3 to 6 months. All but 1 of these firms reported they were already engaging with the PDP team about the interface they were planning to build, with the 1 remaining firm reporting that they planned to do so in the next 3 months.

5.1.4 Number of parts to connect

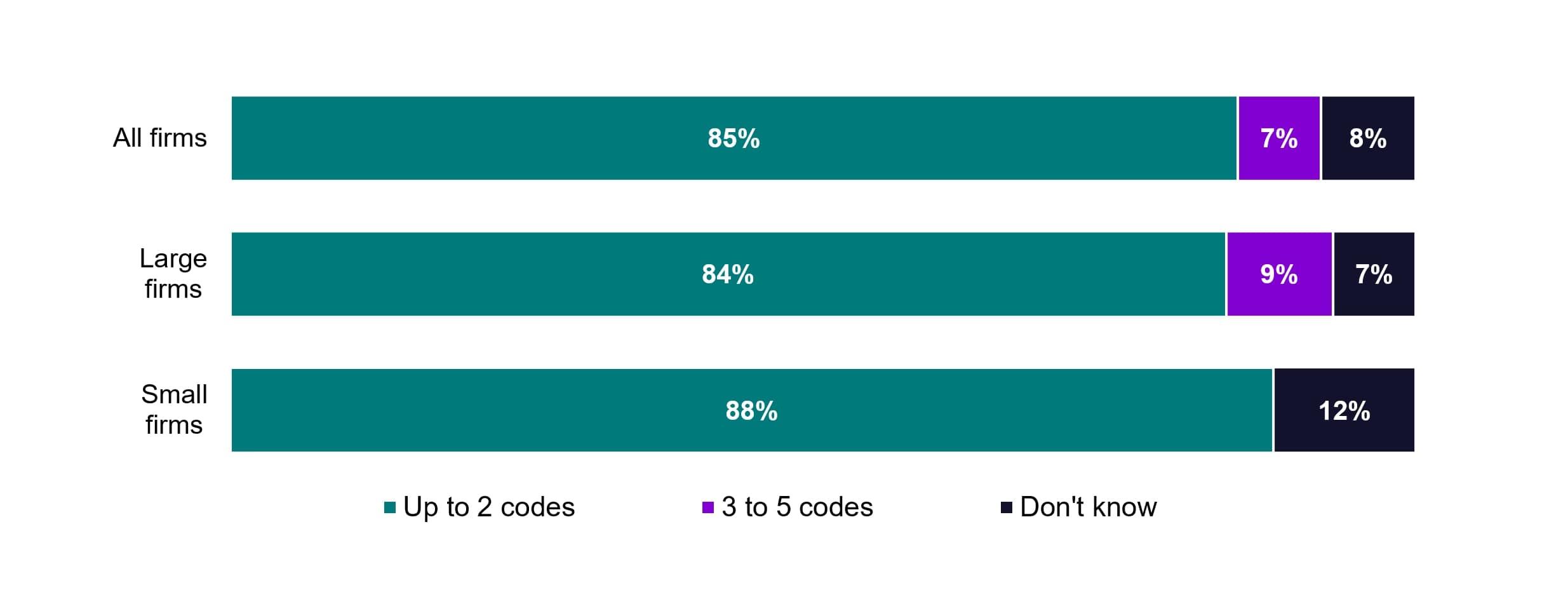

To connect, firms require ‘registration codes’ issued by the FCA and provided to PDP during the connection process. Where a firm has different parts that connect separately, it needs a code for each part meaning that some firms will need multiple registration codes. More than 8 in 10 firms (85%) reported they anticipated needing no more than 2 registration codes to connect, while only 4 firms reported they anticipated needing more than 2 codes (all of which were large firms). No firms reported that they anticipated needing more than 5 codes (Figure 5.3). Just 5 firms did not know how many codes they would need, amounting to 2 small firms and 3 large firms.

Figure 5.3 How many registration codes firms intend to use

(C17) How many registration codes do you currently anticipate needing to complete your connection?

Bases: All (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Up to 2 codes | 85% | 84% | 88% |

| 3 to 5 codes | 7% | 9% | 0% |

| More than 5 | 0% | 0% | 0% |

| Don’t know | 8% | 7% | 12% |

Back to top

6. Preparations and readiness for connection

6.1 Awareness of duties

As part of their duties in relation to pensions dashboards, firms are required to:

- connect their pension schemes to a central digital architecture

- use personal data provided by the users of pensions dashboards to search for a match in the firms’ pensions records.

- return the up-to-date pension asset information to any matched customers via dashboards

- do all of the above in line with standards set out by the Money and Pensions Service

Firms’ self-reported awareness of duties was generally very high, with nearly all firms (98%) reported that they were aware of all requirements and regulations set out by the FCA. One firm reported that they were only aware of 1 of these duties, which was the requirement to return the up-to-date pension asset information to any customers of their schemes via dashboards.

Firms were also asked whether they had carried out the following steps:

- Added pensions dashboards as a regular item at board meetings or another executive committee.

- Assigned budget to deliver the work required to prepare for their duties.

- Discussed connecting to the central digital architecture with their relevant administrator or outsourcer.

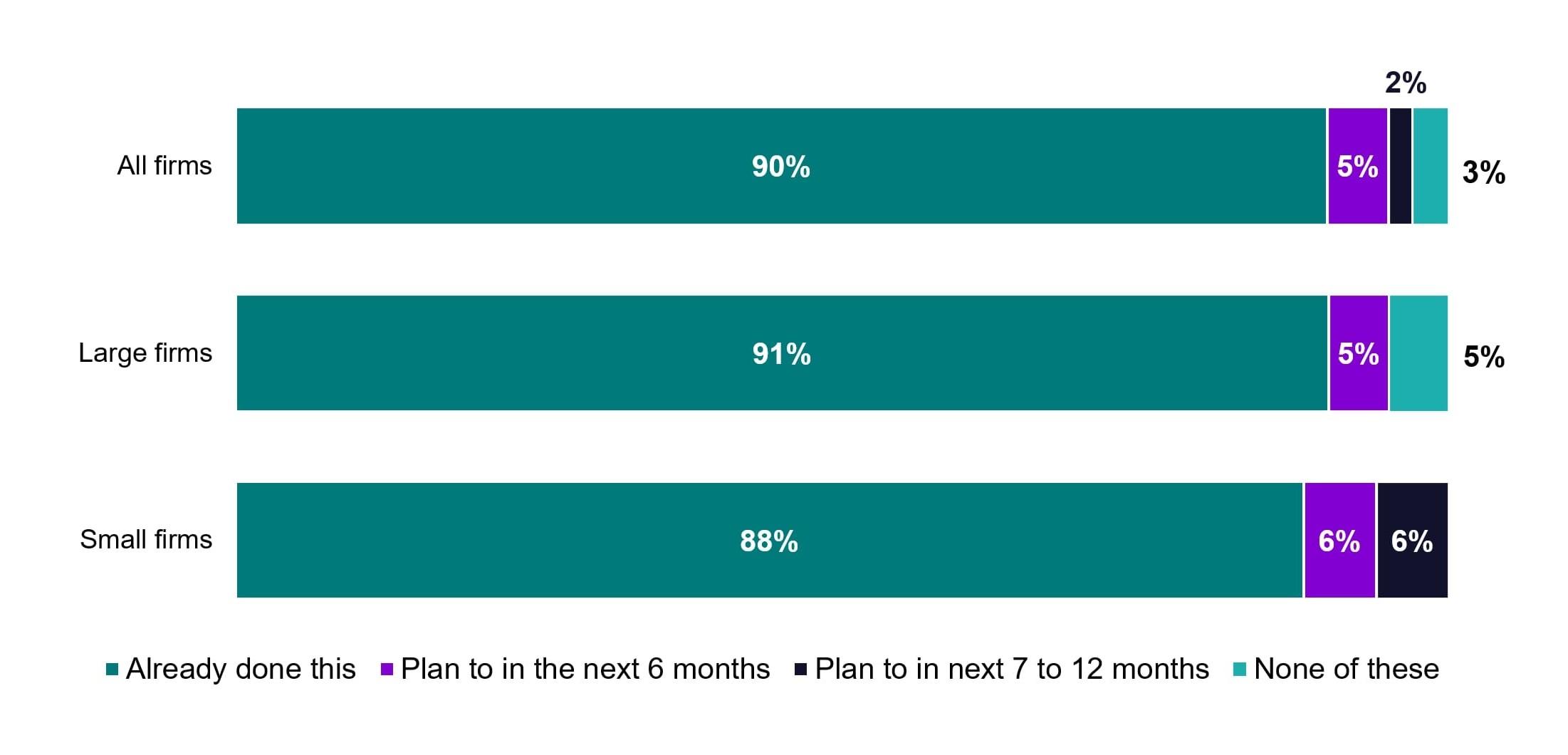

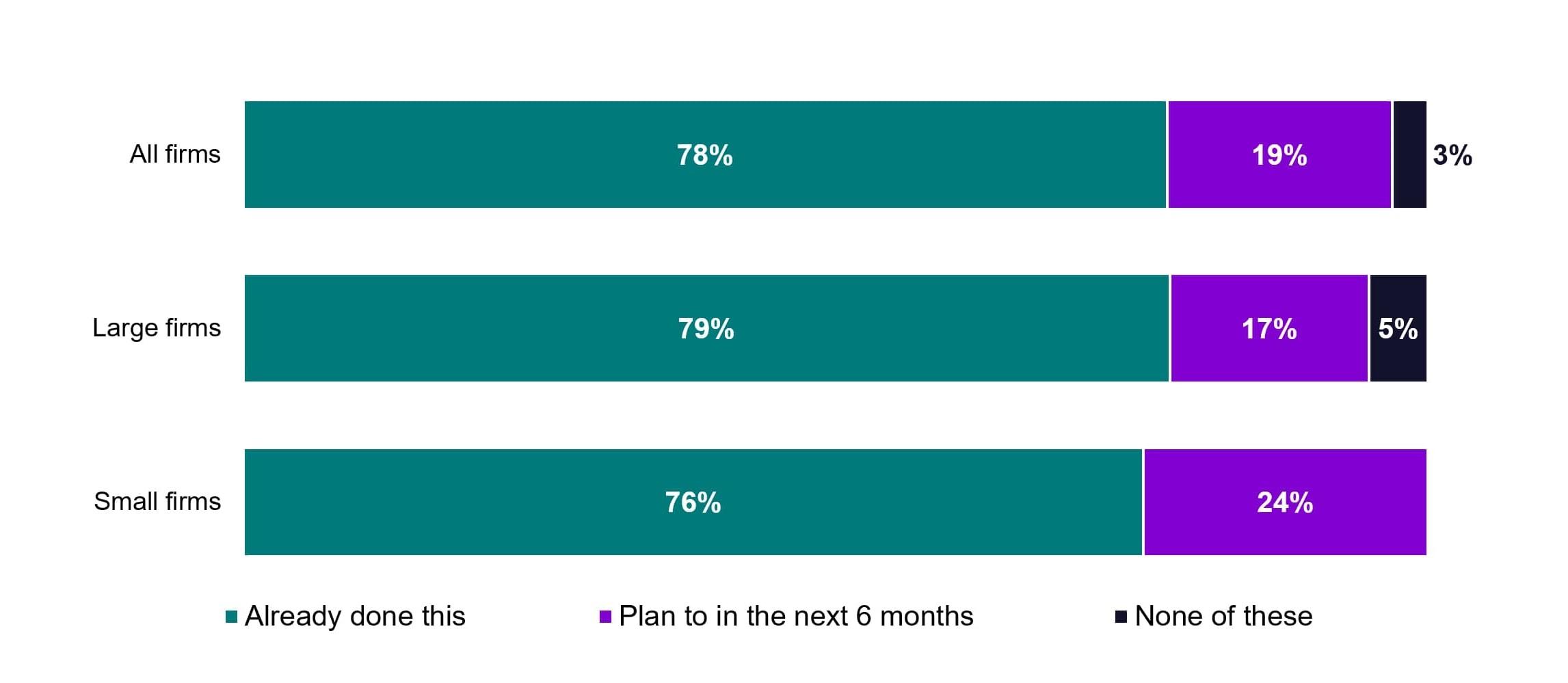

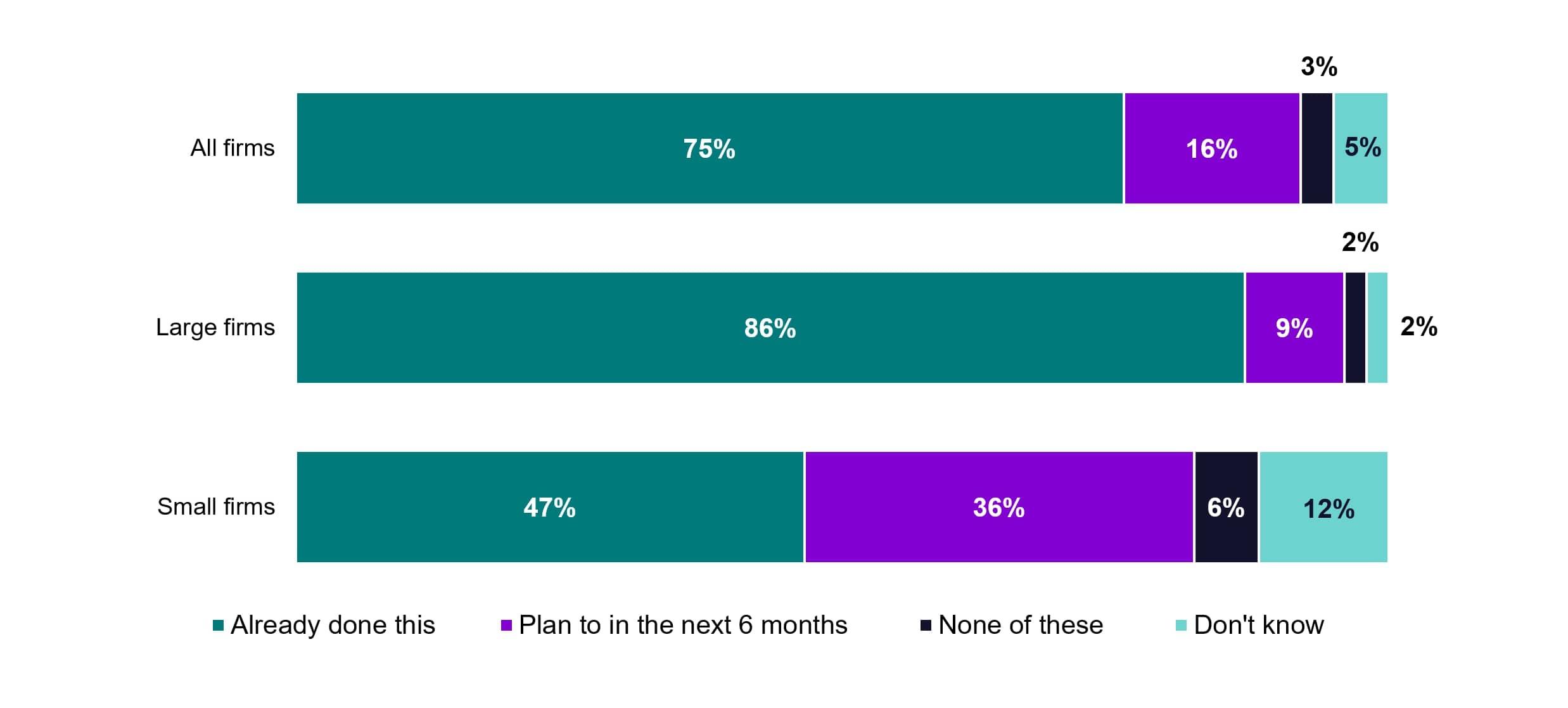

As shown in Figure 6.1a, 9 in 10 reported that they had already discussed connecting to the pensions dashboards central digital architecture with their relevant administrator or outsourcer, around 8 in 10 (78%) reported they had added pensions dashboards as a regular item at board meetings or another executive committee and three-quarters (75%) reported they had assigned budget to deliver the work required to prepare for their duties. In the case of assigning budget, there was notable difference between large and small firms, with around half of small firms (47%) having already assigned budget compared to 86% of large firms. However, most small firms that had not already assigned budget planned to do so within the next 6 months (36%), and only 1 firm reported they did not plan to do this within the next 12 months, whilst 2 reported they did not know when they planned to assign budget. As small firms have a later ‘connect by’ date than large firms, this lower level of preparation was expected.

Figures 6.1a, 6.1b and 6.1c Actions undertaken by firms to prepare for connecting to the central digital architecture

(B3) We would like to understand the level of preparations that are currently underway for connecting to the central digital architecture. For each of the following, please indicate whether you have already done this or plan to do it in the near future?

Figure 6.1a

(B3a) Discussed connecting to the pensions dashboards central digital architecture with your relevant administrator or outsourcer

Bases (B3a, B3b,B3c): All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Already done this | 90% | 91% | 88% |

| Plan to in the next 6 months | 5% | 5% | 6% |

| Plan to in next 7 to 12 months | 2% | 0% | 6% |

| None of these | 3% | 5% | 0% |

Figure 6.1b

(B3b) Added pensions dashboards as a regular item at board meetings or another executive committee

Bases (B3a, B3b,B3c): All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Already done this | 78% | 79% | 76% |

| Plan to in the next 6 months | 19% | 17% | 24% |

| None of these | 3% | 5% | 0% |

| Don’t know | 0% | 0% | 0% |

Figure 6.1c

(B3c) Assigned budget to deliver the work required to prepare for your duties

Bases (B3a, B3b,B3c): All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Already done this | 75% | 86% | 47% |

| Plan to in the next 6 months | 16% | 9% | 36% |

| None of these | 3% | 2% | 6% |

| Don’t know | 5% | 2% | 12% |

6.2 Personal and contact data

6.2.1 Personal and contact data items that will be used for matching

To use a dashboard to access their pensions information, a customer's identity will be verified by an identity service, which will confirm their first and last name, date of birth, email address, and mobile phone number (if used for two-factor authentication). The user’s address will also be checked to exist and have an association with the user. The customer will also be asked to provide additional data to support matching – such as National Insurance number, previous names and addresses, alternative email, and phone numbers. Firms need to be able to ‘match’ customers to their pensions when they receive a find request. Firms are responsible for deciding which data items, from the above list of personal and contact data, they will use to do this.

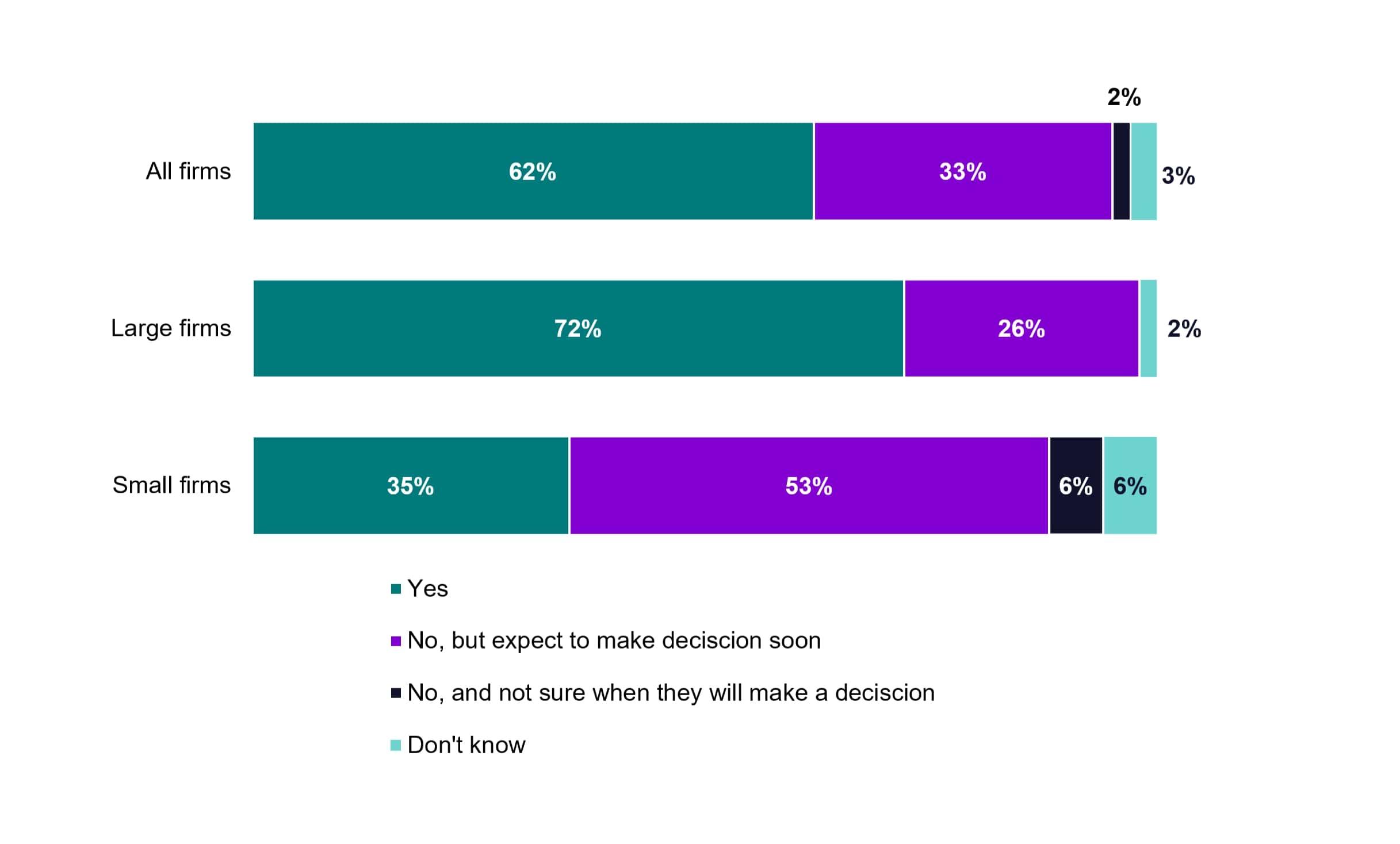

Over three-quarters (72%) of large firms reported already knowing what personal and contact data items they would use for matching customers to their records compared with 6 small firms (35%) (Figure 6.2). However, 9 small firms (53%) reported they were expecting to make this decision soon, with 2 small firms reporting that they did not know which data they would use or when they would decide on this.

Figure 6.2 Personal and contact data items firms intend to use for data matching

(D3) Do you know what personal and contact data items your firm will use for matching customers to their records?

Bases: All (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Yes, have made a decision | 62% | 72% | 35% |

| No, but are expecting to make a decision soon | 33% | 26% | 53% |

| No, and not sure when they will make a decision | 2% | 0% | 6% |

| Don’t know | 3% | 2% | 6% |

6.2.2 Digitisation of personal and contact data

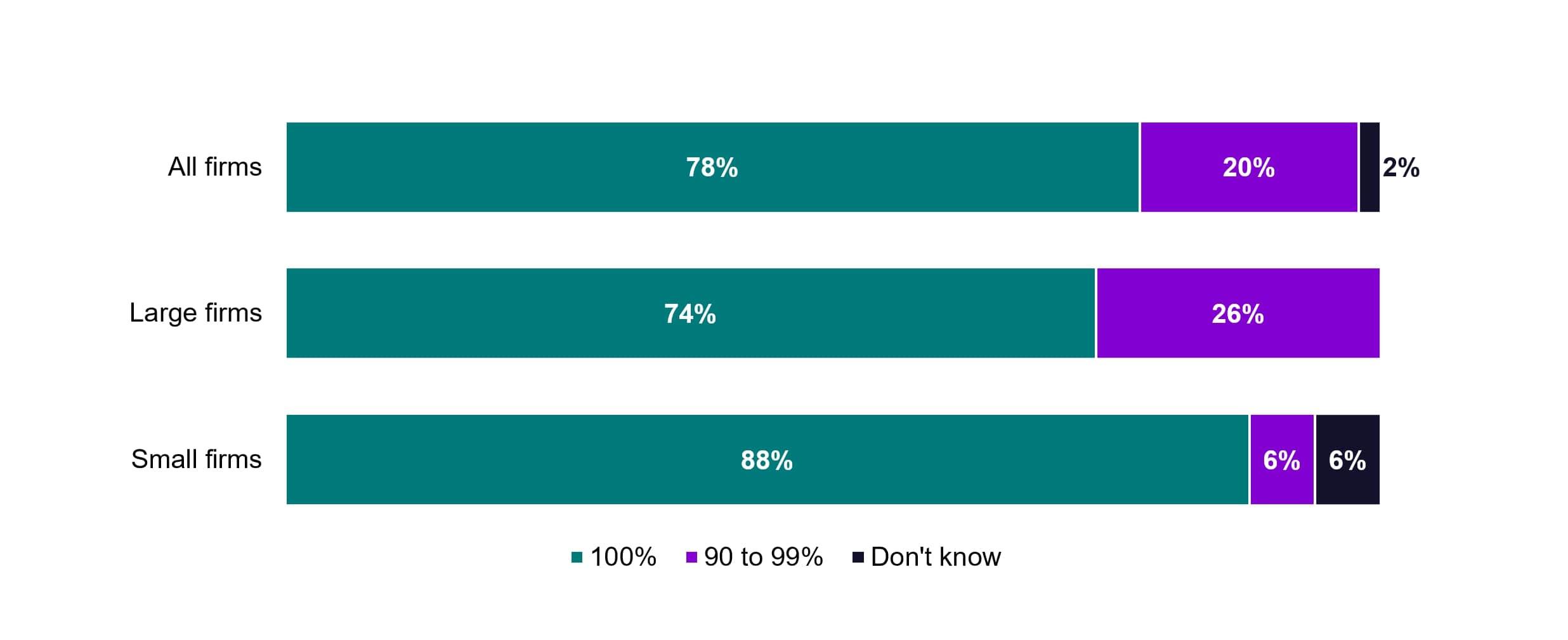

A higher proportion of small firms reported that 100% of their customer personal and contact data was already digitised: 88% compared with 3 in 4 (74%) large firms. (Figure 6.3). One small firm reported not knowing how much of their data was digitised.

Figure 6.3 Proportion of firm's customers' personal and contact data that already exists in digital format

(D1) What proportion of your firm's customers' personal and contact data already exists in digital format?

Bases: All (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| 100% | 78% | 74% | 88% |

| 90 to 99% | 20% | 26% | 6% |

| 80 to 89% | 0% | 0% | 0% |

| 70 to 79% | 0% | 0% | 0% |

| 50 to 69% | 0% | 0% | 0% |

| Less than 50% | 0% | 0% | 0% |

| Don’t know | 2% | 0% | 6% |

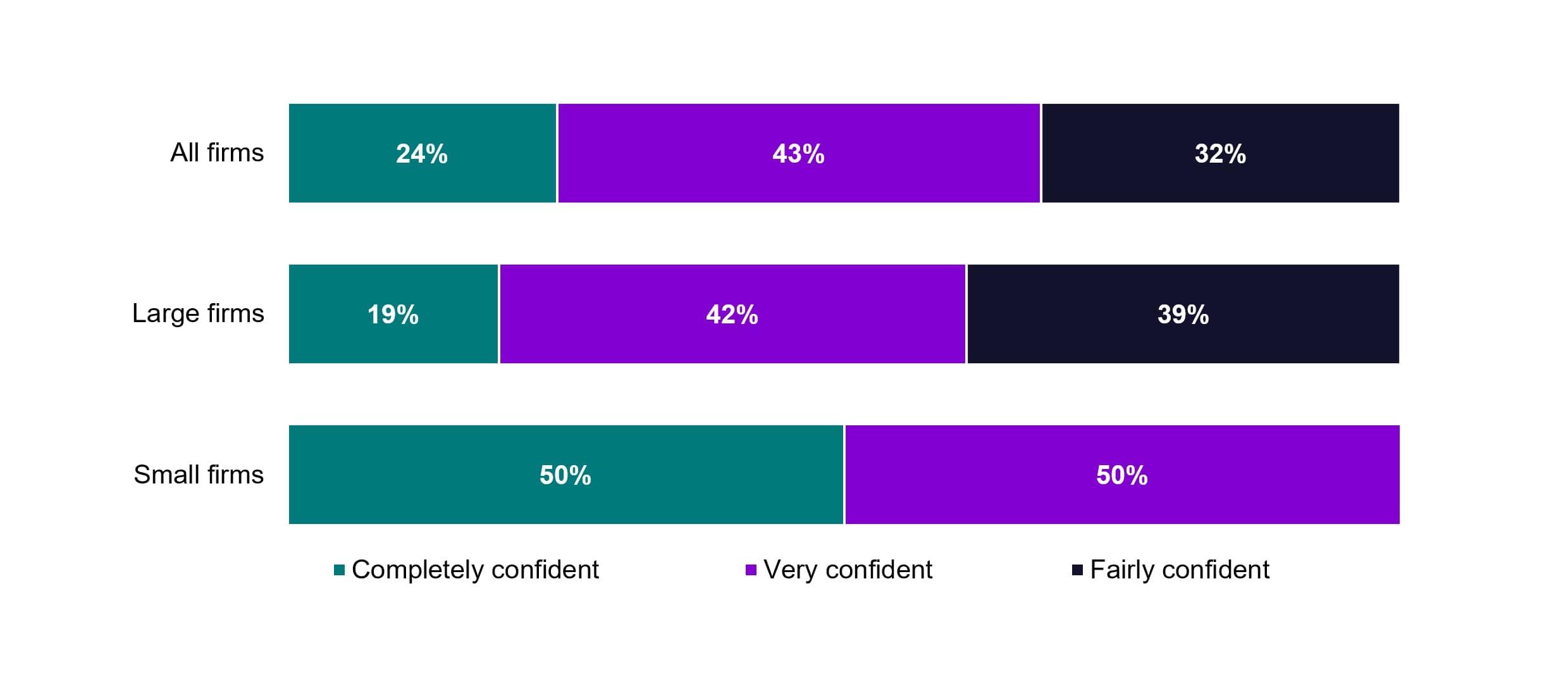

6.2.3 Confidence in accuracy of matching data or personal and contact data

Confidence in the accuracy of data that would be used for matching differed by firm size. All 6 small firms that knew what data they would use for matching and were either completely or very confident in the accuracy of this data (Figure 6.4). Large firms were less confident about the accuracy of this data, 61% reported they were either completely or very confident, the remaining 39% described themselves as fairly confident.

The 21 firms that did not know what data items they would use for matching were asked about their confidence that the personal and contact data they held was accurate. Confidence was very high among these firms, with 9 in 10 (90%) being completely or very confident in their data’s accuracy. Only 2 firms were less than very confident, and these firms both reported they were fairly confident in the accuracy of their data.

The 14 firms that reported they were less than very confident in the accuracy of the data they intended to use for matching, or in the accuracy of the personal and contact data they held, were asked whether there was a plan in place to improve the accuracy of the data they held. Twelve of these firms (86%) reported that there was, and only 2 firms reported they did not have a plan to improve this accuracy.

Figure 6.4 Firms confidence in the accuracy of their matching data

(D4a) How confident are you that the data your firm holds in your records which you will use for matching is accurate?

Bases: All who know what items will be used for matching (37), Large firms (31), Small firms (6*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Completely confident | 24% | 19% | 50% |

| Very confident | 43% | 42% | 50% |

| Fairy confident | 32% | 39% | 0% |

| Not at all confident | 0% | 0% | 0% |

| Don’t know | 0% | 0% | 0% |

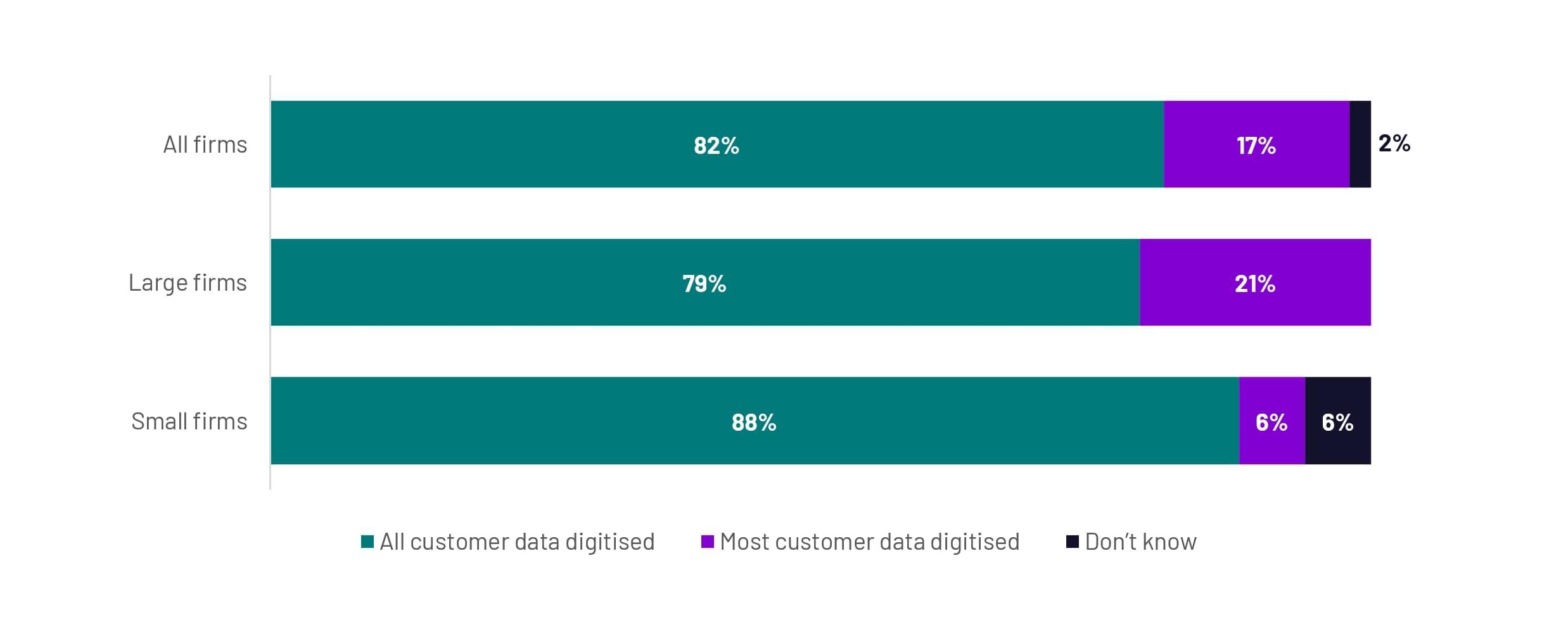

6.2.4 Digitisation of matching data

Over 8 in 10 firms (82%) reported they already had all of the matching/personal and contact data they held for customers digitally (Figure 6.5). Almost all other firms (17%) reported that this was the case for most of their customers’ data, with 1 firm reporting they did not know how much of their customers’ data was in a digital format.

The 10 firms with less than all of their data digitised were asked if there was a plan in place to digitise all of it ahead of their ‘connect by’ date. Eight of these firms reported that there was. These firms were also asked how confident they were that they would be able to achieve digitising this data ahead of their ‘connect by’ date. Five reported that they were confident. Only 2 firms reported that they were not confident in being able to do this, whilst another 3 reported that they didn’t know.

The 2 firms that reported they were not confident were asked to give reasons for their lack of confidence. One of these firms reported that this was because some of the deferred pension products they administered were ‘held on a non-digital system’ but that due to small and falling numbers of that pension product, they intended to extract and send the data to the dashboard rather than sending it directly. The other firm reported their lack of confidence as being the result of relying on customer response to mailings in order to complete some of the data.

Figure 6.5 Proportion of firms that hold matching data in a digital format

(D7) Is the matching data / personal and contact data your firm holds for customers in digital format?

Bases: All (60), Large firms (43), Small firms (17*) * NB: Small base size

| Answer | All firms | Large firms | Small firms |

|---|---|---|---|

| All customer data digitised | 82% | 79% | 88% |

| Most customer data digitised | 17% | 21% | 6% |

| Don’t know | 2% | 0% | 6% |

6.3 Money purchase/defined contribution value data

If firms have matched data, customers can ask to see their pensions information on their dashboard. This ‘view’ data includes information about the value of the pensions they’ve built up (accrued data), and their estimated retirement income. For any money purchase/DC benefits firms are required to provide values calculated in line with the rules set by the FCA and the Financial Reporting Council. If a customer requests to see their pension information ('view' data) and the firm has already provided this information in a statement within the last 13 months or a calculation for the member within the last 12 months, the firm must provide it on the dashboard immediately. However, if the firm has not provided this information recently and needs to calculate it, they have 3 working days from the day after a match is confirmed to provide it.

6.3.1 Calculation and retrievability of purchase/DC value data

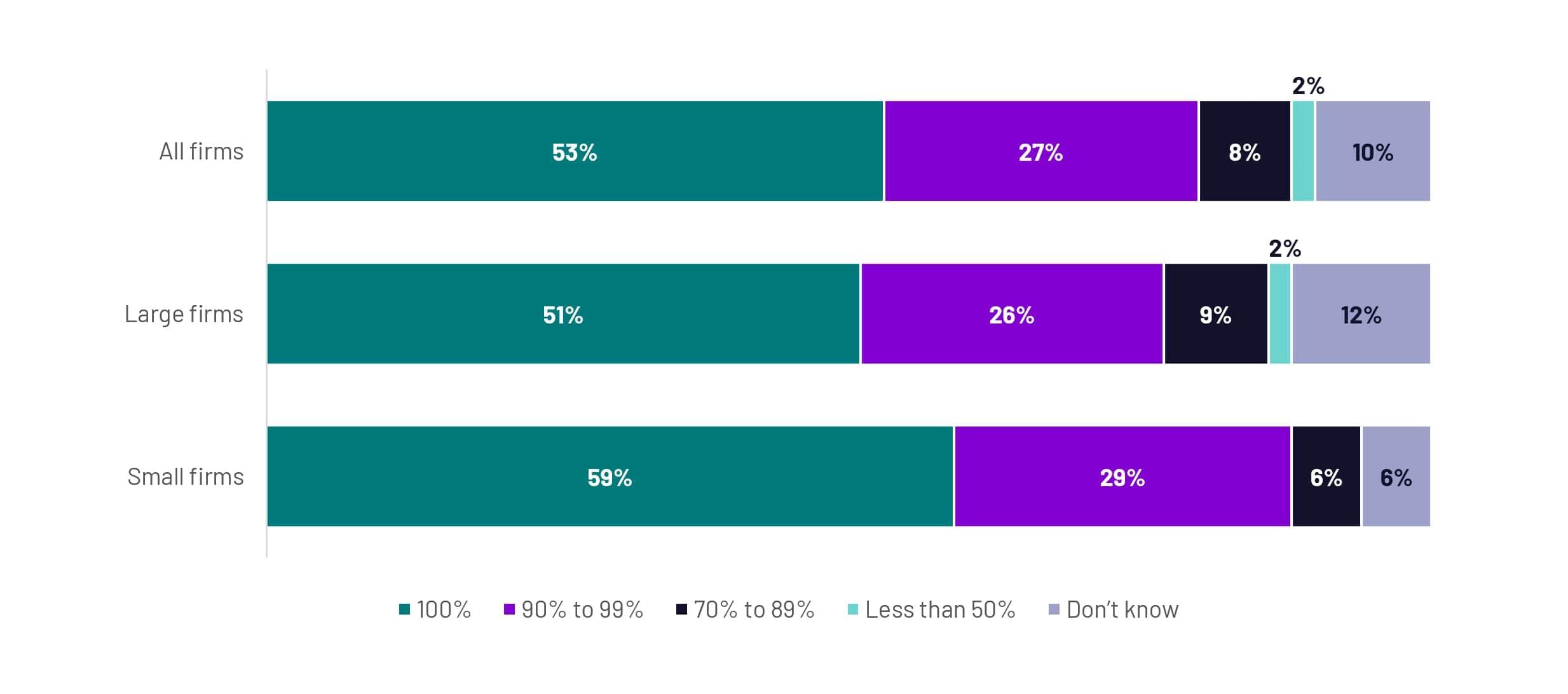

More than half of all firms (53%) reported that 100% of their money purchase/DC value data was already regularly calculated and immediately retrievable, and a further 27% reported that this was true of 90-99% of their money purchase/DC value data (Figure 6.6). Only 1 firm reported that less than 50% of the data was already regularly calculated and immediately retrievable, whilst 6 firms reported that they did not know how much of their data this was true for.

The 28 firms that reported less than 100% of their data was regularly calculated and immediately retrievable, including those who reported not knowing what proportion of their data this was true for, were asked how they planned to calculate the value data. Six in 10 (61%) intended to calculate these values on demand and return them within the required 3-day period, with over 1 in 3 (36%) firms reported that they planned to calculate the values regularly, so they were recent and available on demand. Three firms did not know how they would calculate the value data. Small firms were most likely to intend to calculate the values within a 3-day period, with 5 of the 7 small firms that answered this question intending to do so.

Of all firms, 6 in 10 (62%) were not planning to provide value data that was more up to date than the values shown on the latest Annual Benefit Statement (ABS) or Statutory Money Purchase Illustration (SMPI). Small firms were more likely to intend to provide data that was more up to date (35%) than large firms (23%). The 16 firms that did intend to provide more up-to-date value data were asked what proportion of the pensions they administered would have more up-to-date value data than the latest ABS, to which 88% reported it would be more than 90%.

Figure 6.6 Proportion of firms money purchase/DC value data that is regularly calculated and retrievable immediately

(D11) What proportion of your firm's money purchase/ DC value data is regularly calculated and retrievable immediately?

Bases: All (60), Large firms (43), Small firms (17*) * NB: Small base size

| Answer | All firms | Large firms | Small firms |

|---|---|---|---|

| 100% | 53% | 51% | 59% |

| 90% to 99% | 27% | 26% | 29% |

| 70% to 89% | 8% | 9% | 6% |

| 50% to 69% | 0% | 0% | 0% |

| Less than 50% | 2% | 2% | 0% |

| Don’t know | 10% | 12% | 6% |

6.3.2 Calculation and retrievability of non-DC value data

Firms were asked if they had any non-money purchase / non-DC benefits or hybrid schemes which included a non-money purchase element. Only 9 firms reported that this was the case, with 7 reported that they administered non-money purchase schemes, whilst a smaller number (3) reported administering hybrid schemes with non-money purchase elements. These 9 firms were asked what proportion of their non-DC value data was recent and retrievable immediately, there were a range of responses to this question:

- One firm reported that this applied to 100% of their data.

- Three firms (33%) reported that this applied to 90-99% of their data.

- Three firms reported this applied to 69% or less of their data.

- Two didn’t know much of their data this applied to.

Where non-DC value data was less than 100% of a firm’s value data, firms, including those who reported not knowing, were asked how they planned to calculate this value data. Four firms reported they intended to calculate this on demand within the 10-working day period. Only 1 firm intended to revalue the benefits regularly, but 2 firms planned to use a combination of regular revaluing and calculation on demand. One firm reported that they did not know how they would calculate the value data.

6.3.3 Confidence in meeting value data requirements

There are legal requirements for how pension values must be calculated and how quickly firms must return data to pensions dashboards. If a firm doesn't hold the necessary values, they must calculate and return them within 3 or 10 working days of the day after the match is registered. If a firm already holds the values, they must be returned within 10 seconds of receiving a 'view' request.

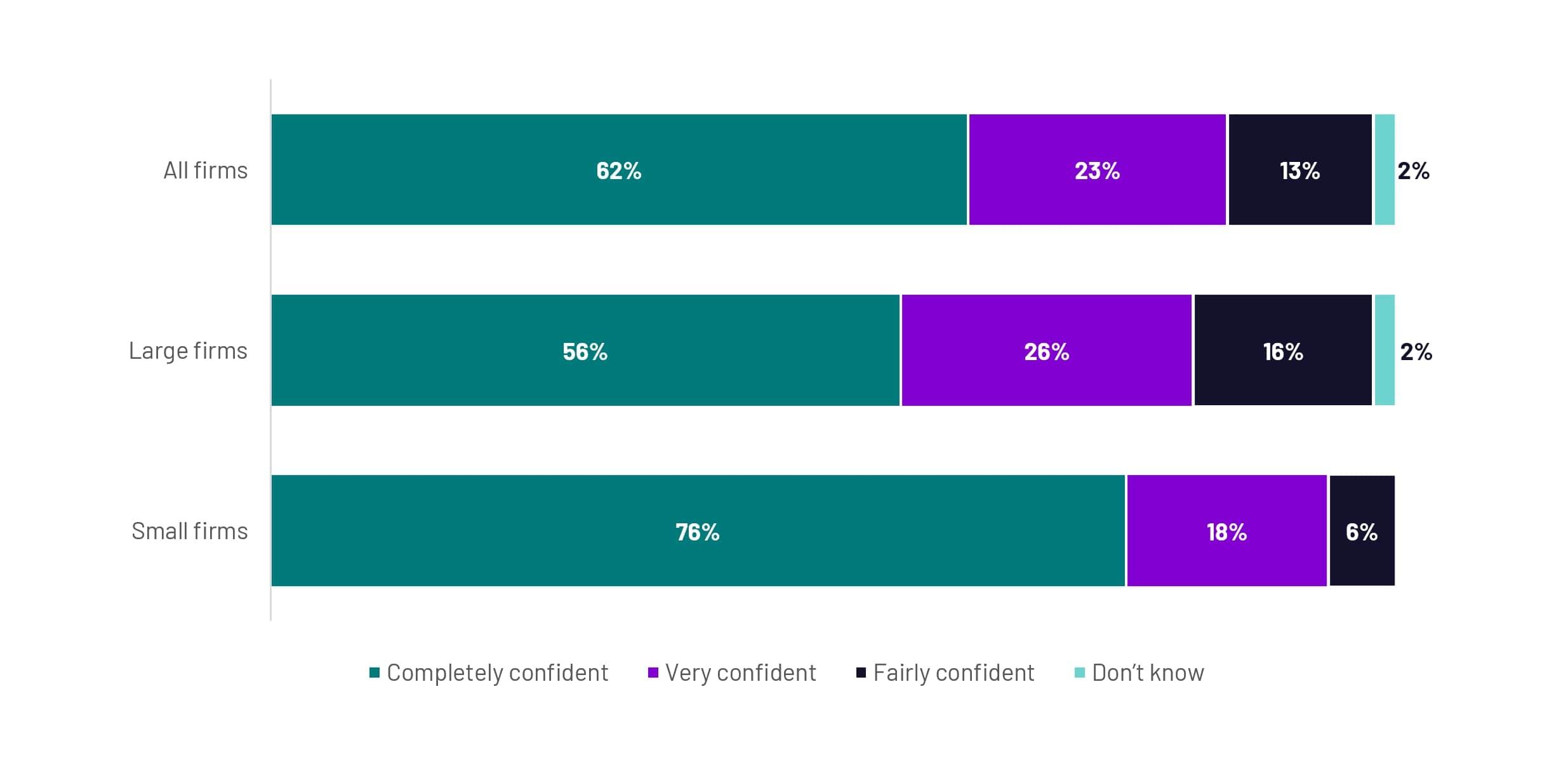

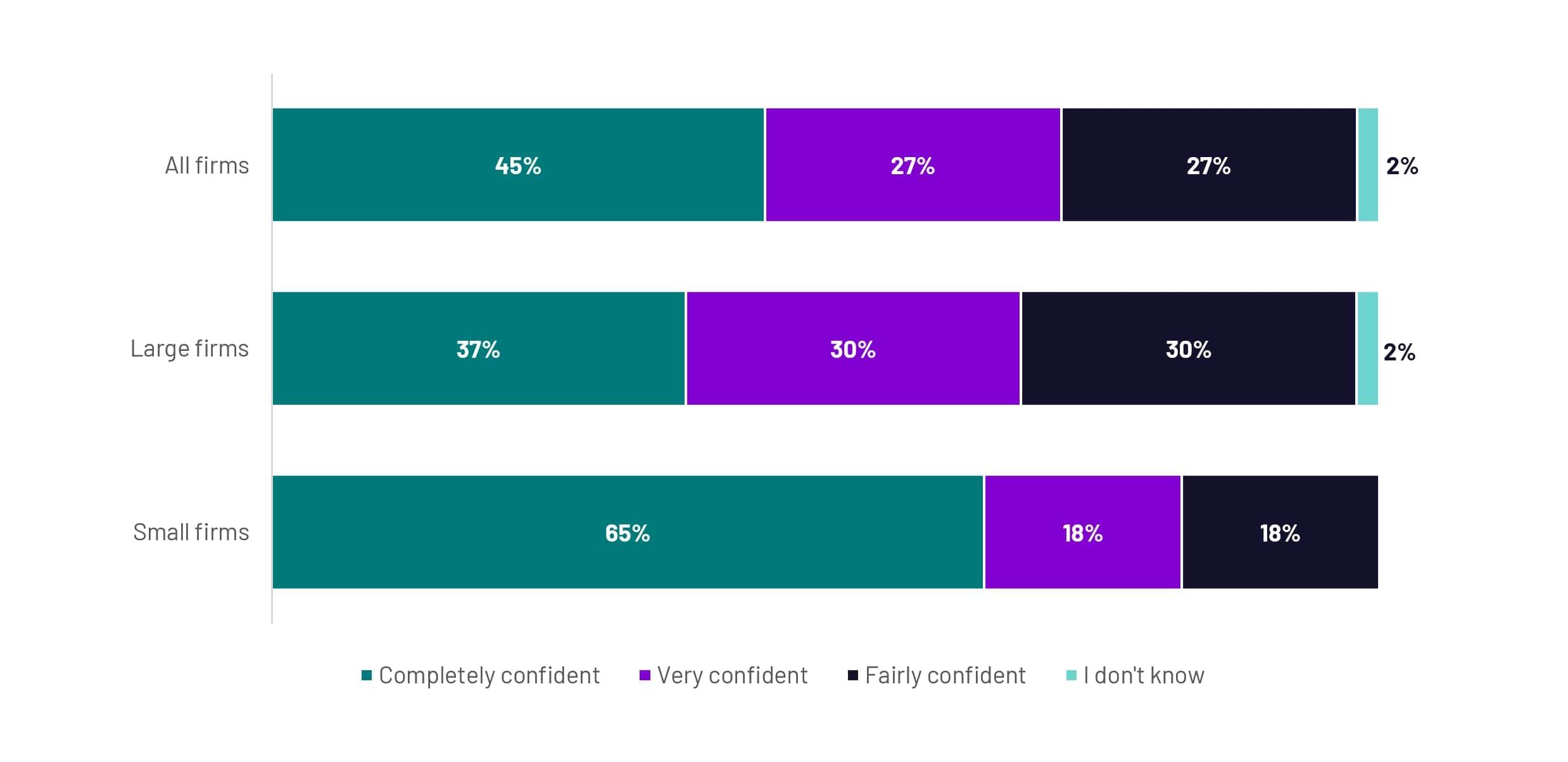

Firms expressed a high degree of confidence in meeting the requirement about how value data should be calculated, with 85% reporting they were either completely or very confident in their ability to do this (Figure 6.7). Firms were slightly less confident, though still expressed a high degree of confidence, in meeting the requirement on how quickly they must provide this data, with 72% reported they were either completely or very confident in their ability to do this (Figure 6.8). No firm reported they were less than fairly confident in being able to meet either requirement, but 1 firm reported they ‘didn’t know’ how confident they were for both cases (Figures 6.7 & 6.8).

Small firms expressed a higher degree of confidence than larger firms in meeting the requirements around how values must be calculated with over three-quarters of (76%) small firms reported that they were completely confident compared to just over half (56%) of large firms. This was even more pronounced for meeting the requirements around how quickly firms must provide data, with around 2 in 3 (65%) small firms expressing complete confidence in their ability to do this, compared to around 1 in 3 (37%) large firms. However, in both cases large firms’ confidence was still fairly high, with 8 in 10 (82%) being completely or very confident in their ability calculate the values to the required standards, and 2 in 3 (67%) being completely or very confident in their ability to meet the requirements around how quickly these values must be provided.

Figure 6.7 Confidence of firms in being able to meet the requirements for how values must be calculated

(D16) For each of the below statements, how confident are you that, from the date you connect, your firm will be able to meet the requirements around… How values must be calculated

Bases: All (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Completely confident | 62% | 56% | 76% |

| Very confident | 23% | 26% | 18% |

| Fairy confident | 13% | 16% | 6% |

| Not very confident | 0% | 0% | 0% |

| Not at all confident | 0% | 0% | 0% |

| Don’t know | 2% | 2% | 0% |

Figure 6.8 Confidence of firms in being able to meet the requirements for how quickly they must provide value data

(D16) For each of the below statements, how confident are you that, from the date you connect, your firm will be able to meet the requirements around… How quickly you must provide the data

Bases: All (60), Large firms (43), Small firms (17*) * NB: Small base size

| All firms | Large firms | Small firms | |

|---|---|---|---|

| Completely confident | 45% | 37% | 65% |

| Very confident | 27% | 30% | 18% |

| Fairy confident | 27% | 30% | 18% |

| Not very confident | 0% | 0% | 0% |

| Not at all confident | 0% | 0% | 0% |

| Don’t know | 2% | 2% | 0% |

6.3.4 Reasons for lower confidence in meeting value data requirements

The 23 firms that reported they were less than completely confident in meeting the requirements gave a wide variety of reasons for lower levels of confidence in meeting the requirements. For confidence levels around how values must be calculated, reasons included the challenges in calculating values of non-standard assets, reliance on third-party administrators, and the application of FRC’s requirements to pensions that were not previously subject to that calculation methodology.

The most common reason for not being completely confident in meeting the requirements around how quickly values must be calculated was reliance on third parties (reported by 8 firms). Other reported reasons included finalisation of internal processes or procedures, the application of FRC’s requirements to pensions that were not previously subject to that calculation methodology and awaiting the completion of end-to-end testing.

(D17a) Why are you not entirely confident that your firm will be able to meet the legal requirements around how values must be calculated?

Some clients that have bespoke SIPPs with us invest in assets that can be difficult to value.

Large firm

We are finalising development calculations for a proportion of our products that need to move from FCA to SMPI calculation.

Large firm

There will be a reliance on third party investment providers and a third-party dashboard provider.

Small firm

We are confident but have not completed the stage where end-to-end testing has provided us with 100% confidence.

Large firm

(D17b) Why are you not entirely confident that your firm will be able to meet the legal requirements around how quickly data must be provided?

Still developing the requirements with our third-party outsourcer. Expect to be entirely confident by the connect date.

Large firm

Until I see the proposed solution and discuss this with our tech supplier, I can't provide a greater level of confidence.

Small firm

We believe we are where we need to be - complete confidence will be reserved for post-testing.

Large firm

Due to the nature of the types of investment that are included in SIPPs, historic issues can impact on sourcing up to date values.

Small firm

6.4 What firms want to help prepare for their dashboard’s duties

6.4.1 Summary

Firms were asked if there was anything they would like to see from the Pensions Dashboards Programme at the Money and Pensions Service, the FCA or TPR to help them prepare for their dashboards duties. The 4 in 10 (43%) firms who reported that they would like further support were asked to give details of this. Responses to this question were varied, but four common themes were identified. Firms wanted:

- standards to be finalised

- more information on the details of what would happen between the deadline and launch of dashboards

- more information on what dashboard screens might look like

- finalised PDP timelines for activities such as onboarding

Details of what is expected to happen between 'connection date' (April 2025) and DAP (currently expected Oct 2026).

Large firm

Regular and realistic updates on PDP’s progress on onboarding schemes by their respective staging dates.

Small firm

We are keen to see a demonstration of the Dashboard, including having sight of the Dashboard screen.

Large firm

How and where the One Login fits in, and visibility of some early screens would be really useful.

Small firm

7. Providing dashboard services

7.1 How firms are planning to provide dashboard services

7.1.1 Intention to provide own dashboard

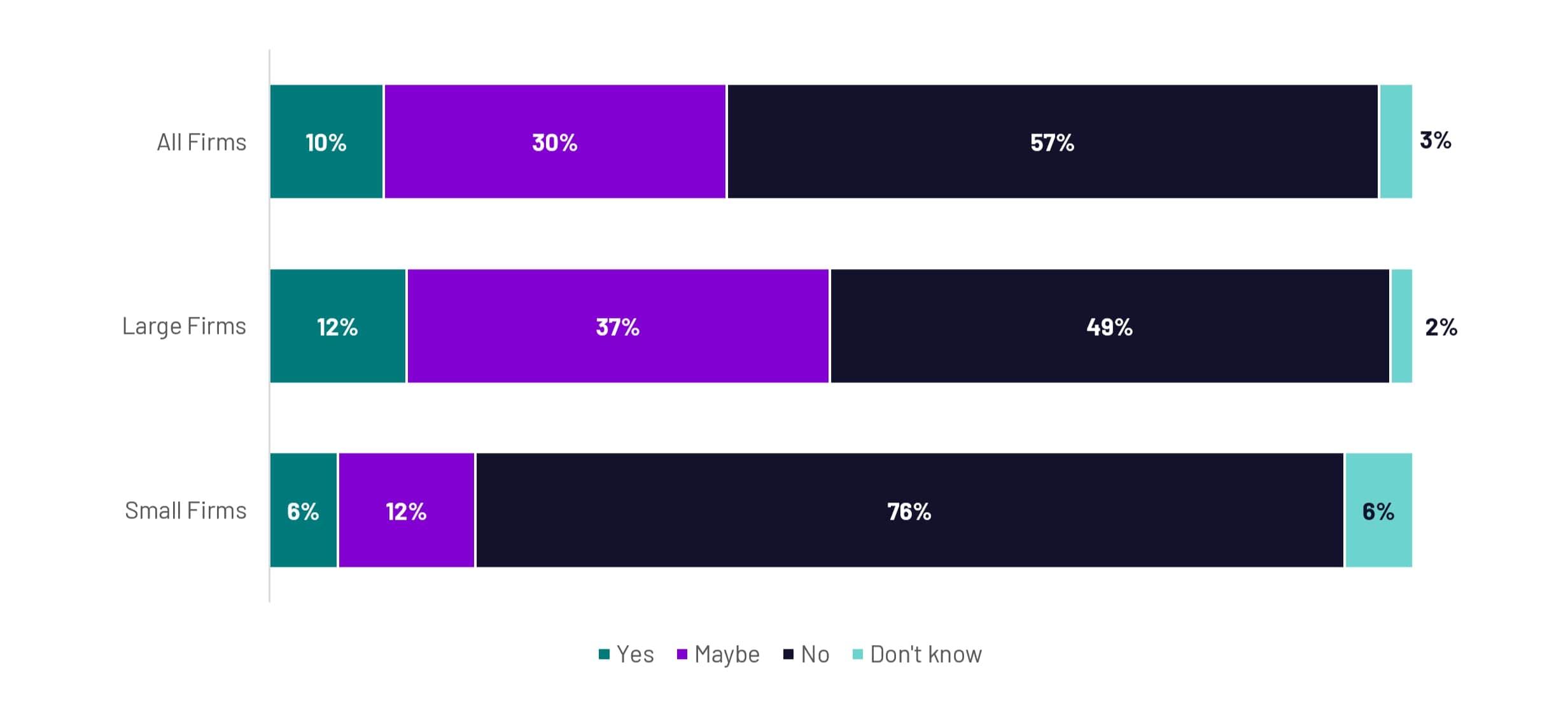

Firms were asked whether they were expecting to provide their own dashboard. Only 6 firms (10%) intended to do this, 3 of which intended to seek authorisation from the FCA to build their own dashboard and 3 of which intended to provide their customers with access to a dashboard built by an FCA-authorised dashboard operator (Figure 7.1). Almost all of these were large firms, with only 1 small firm intending to provide their own dashboard via an FCA-authorised dashboard operator. Nearly 6 in 10 of all firms (57%) had no intention of providing their own dashboard, with small firms being more likely to have reported this (76%) than large firms (49%). Almost a third of all firms felt that providing their own dashboard was a possibility (30%), with small firms again being less likely to have reported this (12%) than large firms (37%).

Figure 7.1 Firms’ intentions to provide their own pensions dashboard

(F1) Is your firm expecting to provide its own pensions dashboard?

Bases: All firms (60), Large firms (43), Small firms (17 *) * NB: Small base size

| Intention | All firms | Large firms | Small firms |

|---|---|---|---|

| Yes - intends to provide their own dashboard | 10% | 12% | 6% |

| Maybe | 30% | 37% | 12% |

| No - does not intend to provide their own dashboard | 57% | 49% | 76% |

| Don’t know | 3% | 2% | 6% |

7.1.2 Intention to promote pensions dashboards

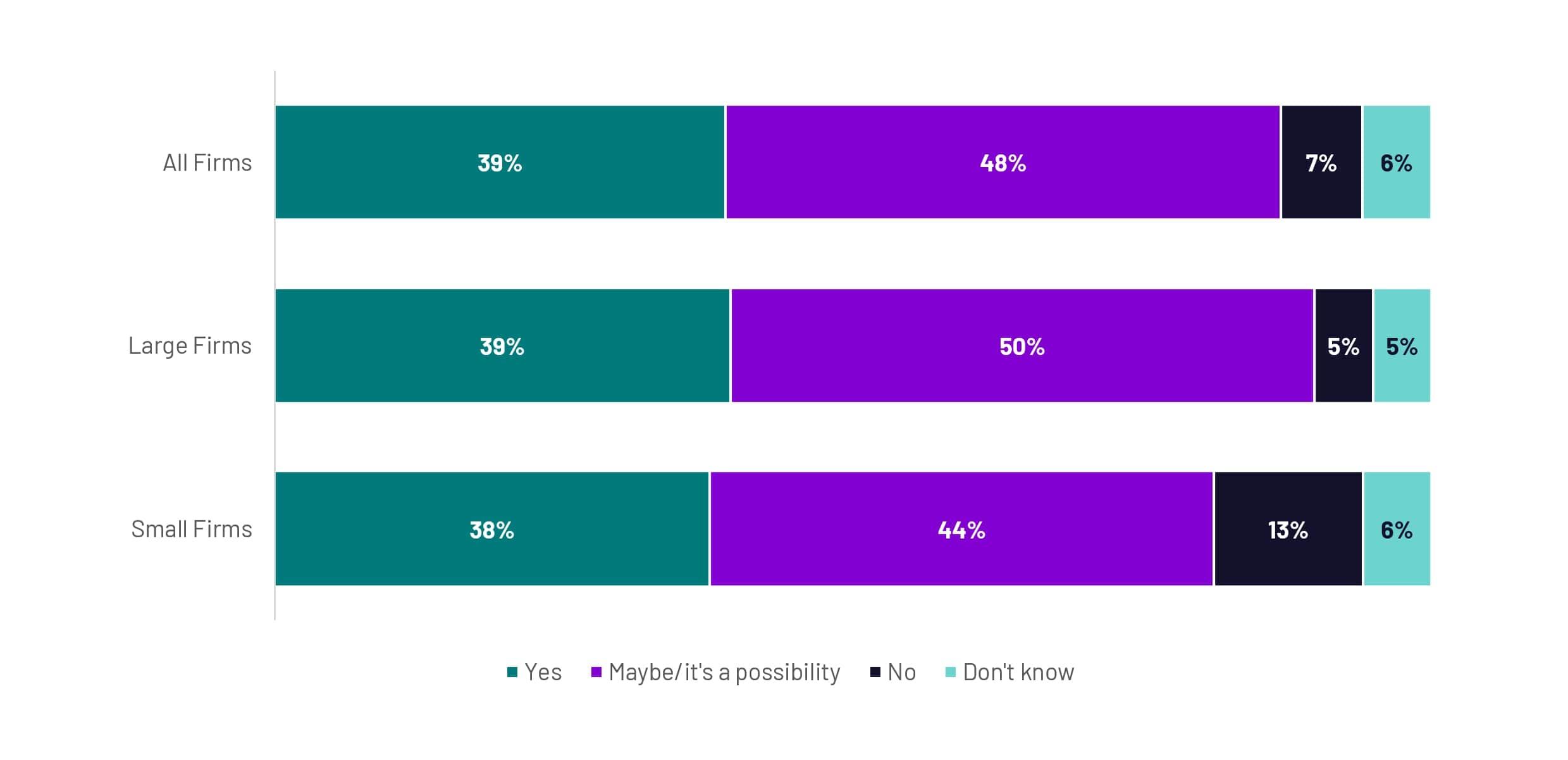

Around 4 in 10 firms (39%) were intending to promote pensions dashboards to their customers, whilst almost half (48%) felt that it was possible that they would do this (Figure 7.2). Only 4 firms reported that they would not do this.

Figure 7.2 Firms intentions to promote pensions dashboards to their customers

(F2) Is your firm planning to promote pensions dashboards to its customers?

Bases: All firms (60), Large firms (43), Small firms (17*) * NB: Small base size

| Intention | All firms | Large firms | Small firms |

|---|---|---|---|

| Yes, is planning to | 39% | 39% | 38% |

| Maybe/it’s a possibility | 48% | 50% | 44% |

| No, is not planning to | 7% | 5% | 13% |

| Don’t know | 6% | 5% | 6% |

Back to top